Journal #1- 10/06/2021

Snippet, Good Reads, Thoughts Around Markets and Portfolio Updates

Hey! My original thought when I started this blog was to share literally everything that I do and gather around Markets like Notes, Thoughts, Insights, Actions, Resources and Research. Over last 2 months or so, I have mostly written and shared insights on my frameworks and research around few stocks.

Through this Journal Series I am looking to cover additional areas like Resources, Thoughts, Actions etc. These would be recurring posts wherein to begin it would have 4 sections,

Snippet

Good Reads

Thoughts Around Market

Portfolio Updates

I’ll look to add more sections over time to accommodate more of my day-to-day activities around Full-Time Investing.

Snippet

This snippet aptly highlights one of the biggest challenge most investors face in the market, which is to keep distance from Hot themes in the market. FOMO (fear of missing out) on sharp rise in such hot stocks results in investors buying into stocks without proper rational at the peak fundamentals and peak stock price (the only rational is continued expectation of rising stock price) and then ending up with major losses. The chart highlight themes that ended up becoming the FOMO themes in previous bull markets.

The latest one is quite interesting- which is basically every stock in the market. I think with the benefit of hindsight everyone has regrets of not buying enough in March 2020 😅

Good Reads

1.Startup Ecosystem

Latest quarterly letter from Hayden Capital (LINK) provides some good insights on development of Startup ecosystems in a country.

The letter highlights the initial challenges faced by the 1st Generation startups which includes-

1. Talent Constraints- As people are skeptical about working for a smaller company with a new business model.

2. Funding Constraints- Initially there is lack of local venture community and without a precedent of successful exits, the global funding is also limited.

3. Regulatory Constraints- Regulatory framework does not exists to accommodate the new business model of startups.

4. Lack of Demand- Being a new product/service, there is a lack of existing demand or say market for the product/service.

But even though the journey is tough, some of the 1st generation companies are able to make it past these hurdles to become globally known firms and valued at billions of dollars. These companies act as a platform and lays the foundation of 2nd Generation of startups as,

Success of 1st Generation companies makes it easier for talent to accept the possibility that leading business can be created from scratch and with a larger wave of 2nd Generation companies, the demand of talent is also wider which in turn attracts talent that was earlier moving to global markets.

On the funding side as well, the 1st generation companies create a lot of wealth for founders and early employees who take this new wealth and reinvest them back into the 2nd generation of startups. Plus, success of 1st generation companies acts as signal to global investors that there is a viable opportunity to create wealth in the region.

1st Generation companies also makes it easier for 2nd Generation companies in terms of a ready market base as 1st generation companies would have already created an environment of rapidly growing consumer base that is interested in such new products/services. Like Flipkart created an e-commerce ecosystem which allowed for logistics startups like Delhivery a growing market base or say a Direct-2-Consumer brand that can tap into the customer base available of e-commerce websites like Flipkart.

The letter further expands on how this played out in China wherein the 1st Generation startups like Baidu, Alibaba and Tencent started around 2000 and then a decade later the 2nd Generation startups like Meituan (2010) and Bytedance (2012) launched in a more developed ecosystem.

And this is very relatable to what we are seeing in India. 1st Generation startups like Flipkart, Zomato, Paytm etc started in around 2007-2008s and the success of these startups have paved way for 2nd Generation of startups like Curefit, Udaan etc almost a decade later in 2016-2017.

This would be a good read for all investors as we are going to see many of the 1st Generation startups come up to public markets this year.

2. All Revenue Is Not Created Equal

This article (LINK) explores one of the key principles in the market that more than quantum, it is the quality of revenues/profits that is important. Two companies with same level of revenues/profits might have extremely different market caps, because Business is just one part of GAME OF STOCKs, what valuation the market prescribes so such business is an equally important part.

The article lists some key attributes that determines the quality of Revenues, so as to get to a so-called club of stocks that are valued at 10x their sales.

Some of the good points-

1. Visibility/Predictability are Highly Valued- Market values secular and predictable business higher than a volatile business. Most SaaS companies get 10x their sales as market cap largely due to their subscription-based annuity type revenues. On the other hand, one-time revenues are not really valued by the market.

2. Margin Levels- This a very important concept that one should really pay attention to, a company like Team Lease will not be valued as highly given that 95% of its revenues is basically a pass though of employee costs that it collects and pays.

3. Marginal Profitability- If a business is such that incremental revenues will generate even higher incremental profits because there are no major costs attached to incremental business, than such revenues would be highly valued. This is the very reason why Platform businesses are valued much higher.

4. Organic- Organically generated revenues will be more valuable than revenues generated from higher marketing or through acquisitions.

Thoughts Around Market

One thing I have observed over last couple of weeks is that market has become extremely aggressive in discounting. There are so many stocks that have jumped 50%+ within 10-15 days of their results. And it is not just the speed at which the possible future is getting discounted, but even the probability that market is assigning to such possible future actually materializing is huge. It feels like market is ready to give valuations based on profits of 3-4 years ahead today and that too as if there is 100% surety that such profits will come.

Some of the stocks wherein I have observed such movements are Lux Industries, TCI Express, Angel Broking, Ease My Trip and Rupa.

TCI Express is the one that surprises me the most. I have tracked this company for nearly 3 years now, and the management here has always over-guided and under-delivered. This time, they guided that their profits would be 4x in 4 years and market looks to be discounting this with high certainty that they will achieve this, ignoring the fact that in the past the company has always missed the guidance.

So, the Aggressiveness of Market Discounting New Developments is quite Surprising to say the least and is a thought to ponder on.

Portfolio Updates

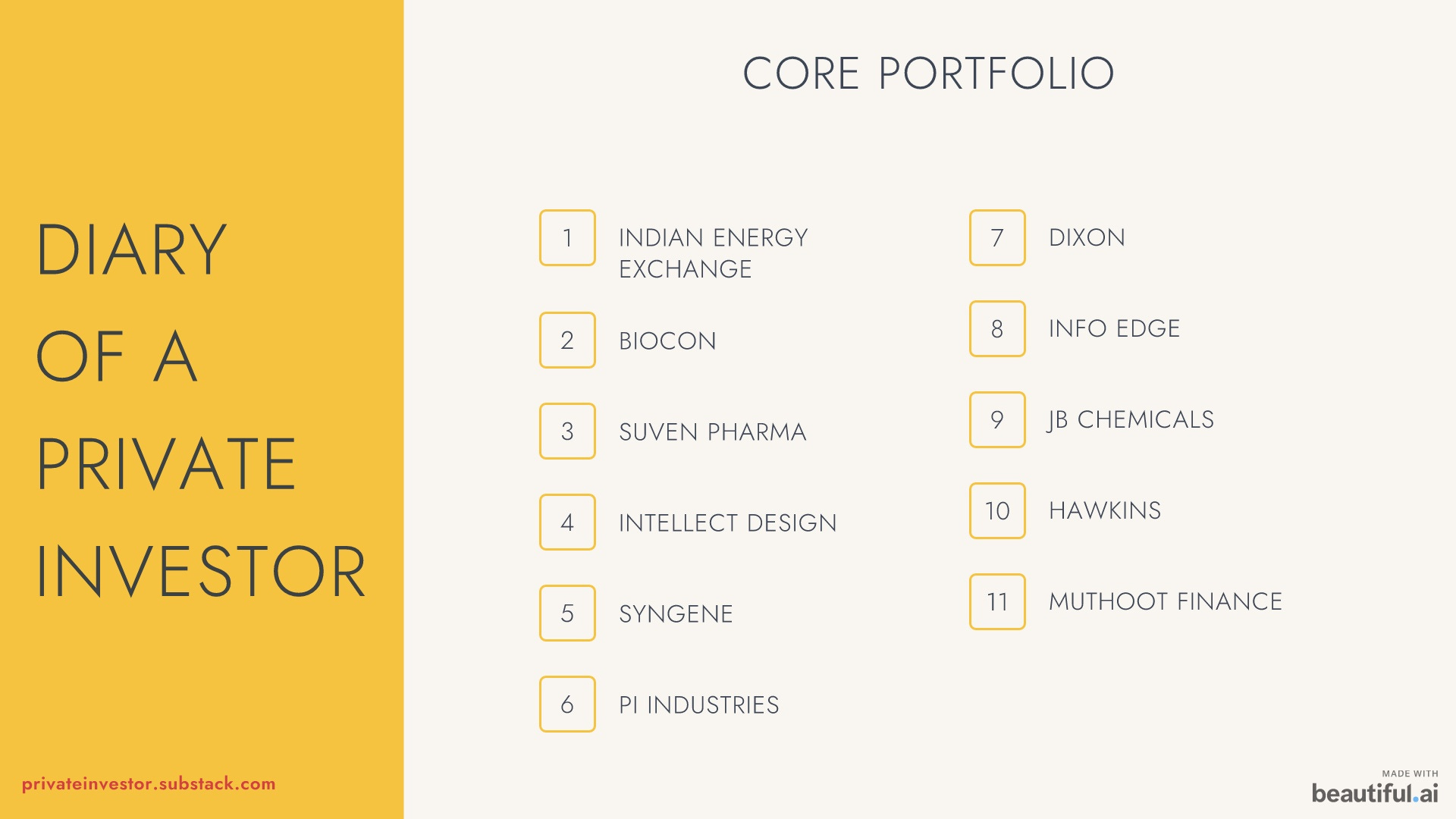

CORE PORTFOLIO

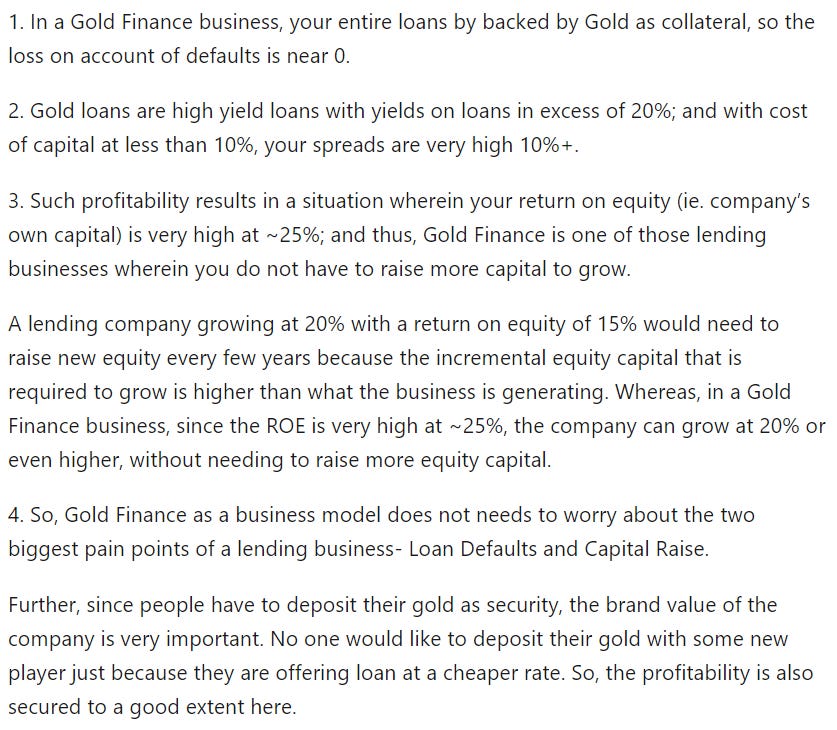

Added Muthoot Finance in the Core Portfolio.

I had talked about why I like Gold Finance business in this post, sharing the snippet from it.

TRENDZ PORTFOLIO

No Change & No Update

That’s All For This One

10/06/2021

Very well written. Thank you for that. My question is why Muthoot? Not Manappuram? Is not TIPS India have stretched valuation at this moment?