How To Find & Evaluate Complex, Non-Linear and Optionality Opportunities

Follow-Up to the Previous Post with Case Study on Suven Lifesciences

In my previous post I had talked about why one should consider Investing in opportunities that are Little Complex, Can Deliver Non-Linear Growth and Have Optionality. If you have not read it yet, I’ll strongly recommend you to read that first (Click Here) before reading this post, as it will give you a better understanding of what I have discussed below.

In this post I want to highlight some key points that can help one Find & Analyze such Opportunities. Also, I’ll describe the case study of Suven Pharma (Erstwhile Merged- Suven Lifescience) on how it reflected on each of those points to help you get an even better and broader understanding.

The reason for choosing this company is because it is one of the rare investment opportunities that had all the three attributes- Complexity, Non-Linearity and Optionality. Plus, I have personally seen It play out for myself and It is the Investment that got me hooked to this framework of Investing.

Get Ready For The Hard Work

I cannot highlight enough the importance of putting proper effort and going deeper into analyzing a company using raw sources. As I had highlighted in the previous post that these businesses are new, different and evolving and thus are under-researched, so you will hardly find any synthesized resources like reports, blogs etc

Even if you find some, it is always better to do the work yourself because even if you are able to Buy based on such secondary sources, you will never be able to Hold the stock in volatile times or you will end up selling too early, without realizing the true possibilities.

Ian Cassel: The amount of work you do on an investment often correlates with the amount of volatility you’re willing to endure.

When I first read about Suven back in 2018, it was an under-research and under-appreciated company; something that I have realized is the best thing you can have in an Investment early on to benefit from the value discovery.

For those of you who don’t know, Suven works in a segment of the pharma industry called CRAMS (Contract Research And Manufacturing Services), which basically involves working with Big Pharma companies in developing new drugs.

Primary reason for Suven being under-research & under-appreciated obviously was that CRAMS was a new & different business, atleast in the Indian context given that not a lot such companies were listed.

CRAMS has become a buzzword in the investing community in last 1 year as Investors have finally understood the business model here- all thanks to few investors who have shared their qualitative understanding in length with everyone. But before 2020, nobody was really talking about CRAMS as a business and its potential.

Secondly, seeing the financials, Suven was a pass for most people. One thing I have noticed is that for most people the first step is a quick look at financials in Screener and unless it is all clear and perfect-like continuous growth, low debt, low working capital, good cashflows, desired P/E etc, it is a pass. But most of the time financials on the face of it does not paints the true picture of what is happening inside.

Financials can be depressed because of multiple reasons-

The company might be investing in future optionalities or doing some huge CAPEX, which can depress margins and ROCE/ROE for few years.

It could be just how the business cycle works for a company wherein growth comes in a step-fashion manner. And Non-linear growth is typically preceded by slow or erratic growth.

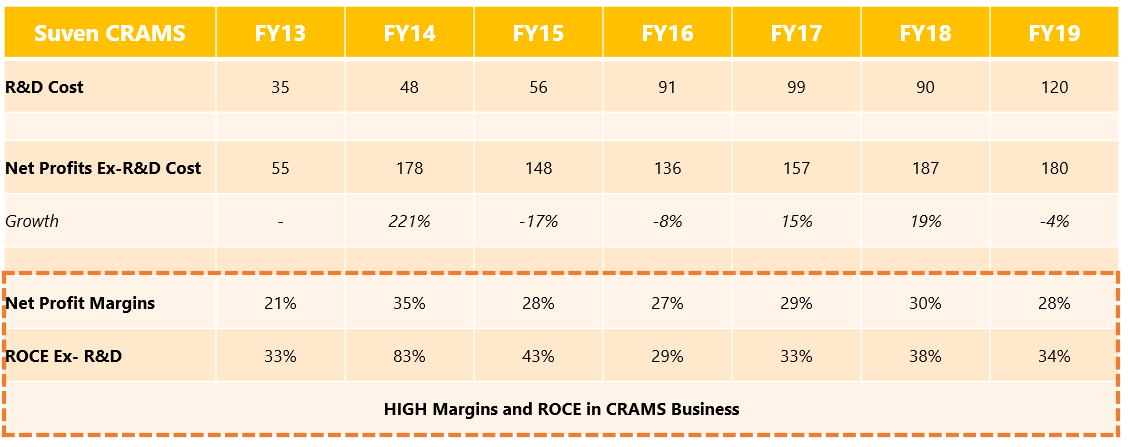

This is how Suven’s financials looked like in 2018-2019. Hardly any revenue growth in recent years and Profitability was too erratic. The financials here were depressed for both the reasons that I have mentioned above-

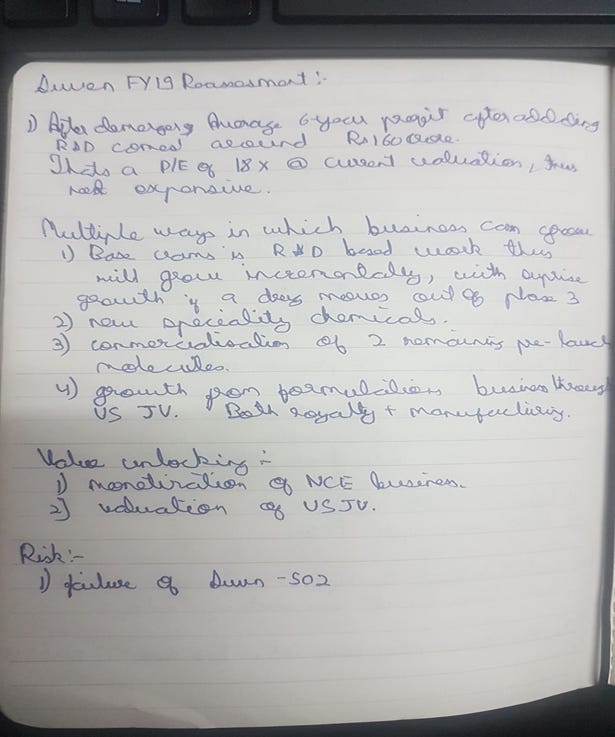

1) Along with its core CRAMS business, Suven was working on its own drugs since 2003, this was the 1st Optionality in Suven.

All the projects in this business were still under R&D stage and were only incurring expense with zero revenues- so basically this business was a drag on company’s core business of CRAMS. And one of its drugs SUVN-502 was in the later stages of its development resulting in higher R&D spends.

If one would have removed the effect of R&D, one could have seen the true profitability of company’s CRAMS business. The business was highly profitable with near 30% PAT margins and 30% plus ROCE.

A 30% PAT margin in a manufacturing business is extremely rare, it speaks for the kind of Value Additive maufacturing a company a doing.

Nowadays, for one thing that Suven is most hilighted everywhere is for its extremely high Net Profit Margins and ROCE (Return on Capital). But, honestly that was always the case; It was only that it was not openely visible due to R&D costs of Drug Discovery business; and only later became clearly visible due to demerger of CRAMS business- the 2nd Optionality in Suven.

2) Growth in Suven’s core business of CRAMS comes in a Step Fashion Non-Linear manner. Even though explaining the qualitative strengths of the CRAMS business model is a separate topic in itself, here I’ll quickly highlight in brief how the business works and why it can deliver Non-linear growth.

CRAMS Business-

So Suven manufactures raw-materials (Intermediates) of drugs which are being developed by Big Pharma company as a contract manufacturer.

Development of drugs happens in stages in which the drug is tested on Humans in clinical trials. And there are three phases of clinical trials- Phase-I, Phase-II and Phase-III. And once a Drug clears all the three phases, it can then be commercialized and be sold in markets to public.

The beauty here is that in each phases the drug is tested on an increasing number of patients. So, phase-I can have 20-100 people, Phase-II can have 100-500 people and Phase-III can have 1000-5000 people. So, with each stage that a drug clears, the requirement for drug multiplies by a factor 5-10x on a small base, resulting in Non-Linear growth.

However, the real growth happens when a drug clears phase-III and is approved & becomes commercial. At this time, requirement of the drug increases from few thousand people in the clinical trials to millions of people who might need that particular drug. And once the use of a drug expands and the Big Pharma company makes it available in more countries, the supplier of raw-materials like Suven benefits from growing demand.

Plus, unlike other drugs which do not have patent and thus can be manufactured by anyone; a new drug has a patent protection and market exclusivity. This is very important because, a Big Pharma will share its patented process with only 2-3 manufacturers and Big Pharma is only focused on the quality of the raw-material and not the cost, given that for a patented drug, it can charge a very high price to the consumers. Thus, a CRAMS player does not face pricing pressure; it competes on product quality.

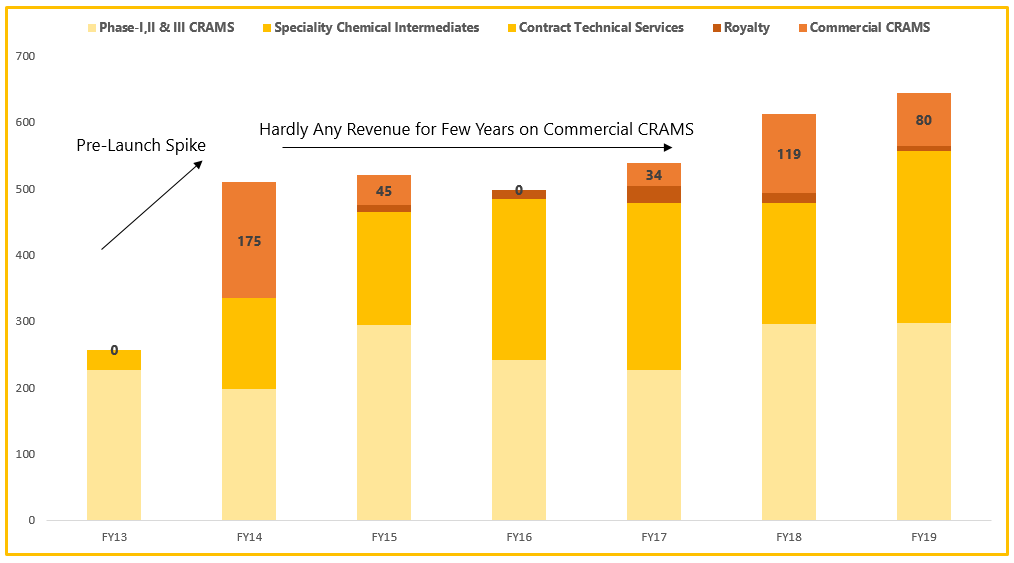

However, when a drug is first approved, the Big Pharma requires huge quantity of drug as a pre-launch quantity and then it takes 1-2 years for a drug to clear regulatory formalities and become available in the market, post which as well, the Big Pharma orders raw materials in bulk every 15-18 months.

This basically results in a situation wherein, when a drug clears Phase-III trails, you have a spike in revenues due to pre-launch quantity order and then new orders for the same starts building up 1-2 years later, that too in batches.

Same thing played out in SUVEN as well. In FY14, 3 drugs on which Suven was working with Big Pharma cleared Phase-III Trials and Suven got huge pre-launch order. Its revenues doubled from Rs250 crores to Rs500 crores in just one year. Post which the revenues from these molecules was not there for next 2 years and thus growth looked shallow, even though revenues from its remaining business was growing.

This aspect of the business dynamic would have been known only if someone would have done through reading to understand the business dynamics. It is only through thorough work will you be able to get a sense of business strength and its future possibilities.

Look for Astute Management

Management quality is important in any investment, but the importance of management is even more when we are looking to invest in Optionalities. Because Optionality is uncertain in nature, a lot of it depends on management’s ability to identify and capitalize on Optionalities.

One would ask how to judge a Management’s quality? Well, there is no straight answer to it.

One has to develop an ability to judge management; like how in our social interaction we are able to get a sense other person’s ability and character based on their conversations and actions, similarly I think overtime every investor is able to get a sense of a management’s ability and character, based on management’s actions and talks; even though personal biases does cloud one’s ability to consider the opposite view at times.

But one thing that I’ll definitely say is that, no one would be able to get it right 100% of the time. Like how there is a fine line between passion and foolishness- If someone doing something out-of-the-box succeeds, then people call it passion and if that person fails, then it is termed as foolishness. Similarly, if a management talks big things, talks of something new & visionary, and then succeeds on it, people would call them Intelligent Fanatics and if they don’t then they are looked at with extremely opposite view.

Few Key Pointers for judging management from the Optionality point of view-

In case of Suven, these qualities were visible. Suven is led by Mr. Venkat Jasti and he has been instrumental in my investment in Suven, because it is through his explanations in Suven’s concall and annual reports, was I able to understand the strengths of the CRAMS business. I think anyone who wants to understand CRAMS business, concalls and Annual reports of Suven should be the primary reference point.

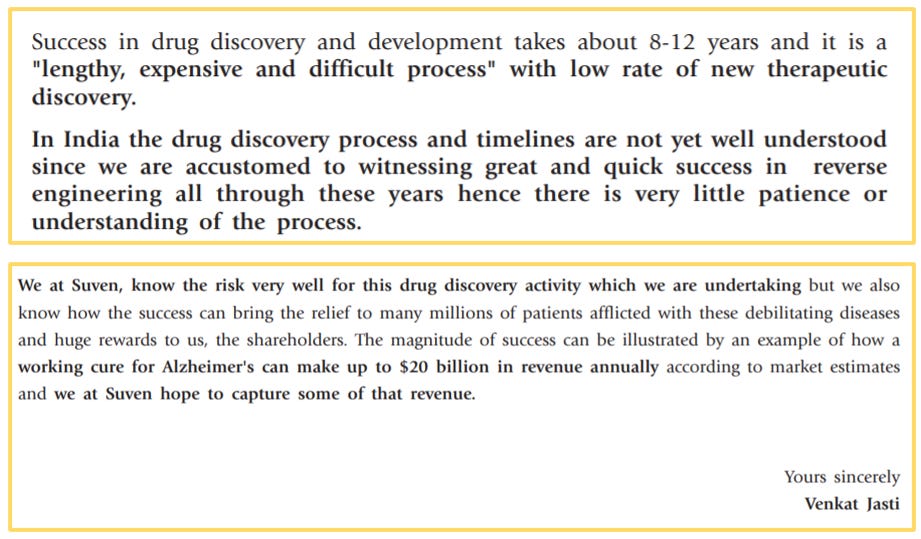

Some snippets from Suven’s early Annual Reports, wherein Mr. Jasti talks about Risk & Rewards of Drug Discovery, showing that he understood Probabilistic and Optionality thinking.

And It felt very natural to me that Mr.Jasti could understand the optionality of drug-discovery business and had the skillset to capitalize the same, given that he had an inside view of Big Pharma companies discovering new drugs as he was helping them do it, through the CRAMS business of Suven. Plus, he had resources in the form of profits from the CRAMS business, which was being invested in the drug discovery R&D. Suven in last 20 years has spent close to Rs1000 crores in its Drug discovery business, largely funded by the profits of CRAMS business.

In my previous post (See here) I had given example of JIO as an optionality for Reliance. There as well, we saw the same thing. Mukesh Ambani was the one who was actually running Reliance Telecom before family split, so he had an inside view of the telecom business. It is even widely reported that telecom was Mukesh Ambani’s dream project and he wanted telecom as well at the time of split. Further, Mukesh Ambani had all the resources from Reliance’s Oil business to fund Jio with 1.5 lakh crores.

So, with a forward-looking mindset, ability to be patient, ability to understand the risks, having an inside view and also the resources; Suven’s management checked all the boxes of a management capable of Identifying and Executing on Optionalities.

Dynamic Industry

Complex, Non-Linear and Optionality opportunities are largely available in Knowledge Based and New Age businesses. Look for industries that strive on innovation; because innovation is what will create new business models and offerings that did not existed earlier.

It is the new business models wherein increasing adoption creates Non-Linear growth, whereas Innovation is what allows for Optionalities.

In the previous post we talked about Music Streaming, here it is the increasing adoption of Streaming business that is resulting in strong growth for Tips Industries and Saregama. So new Business models are good place to look for such opportunities.

Pharma and Tech space is fertile ground for finding such opportunities, both these industries have large opportunity size and have continuously evolved over the years and both these industries are among the top spenders on R&D.

Suven being in the Pharma space had the opportunity to move into newer business models. First with CRAMS in 1995 and then in Drug Discovery in 2003. Both these businesses are complex and provides for Non-Linearity and Optionality.

This again is a testament of Mr.Jasti’s zeal to keep looking for new opportunities and that he is not satisfied with status quo.

Evaluate The Size of Optionality and Risks

When you are evaluating the future possibility of a Non-Linearity and Optionality, getting a sense of the size of such non-linearity and optionality relative to the current business of the company is important. Getting into a new product or geography is an optionality in definition; but if the opportunity is too small compared to current size of the business, then it is not an optionality in real sense as it would not be able to provide a non-linear growth.

Higher the future value of optionality relative to the business’s existing size, the better it is.

Along with Size, getting a sense of the risks associated with an Optionality not playing out is also very important. And the best way to understand this is to ask two questions to yourself-

1.How much of the Optionality is being discounted by the market currently?

Because if the market is already discounting the Upside of the Optionality, then the Risk:Reward is not in your favor. The upside is already discounted and you are taking the Risk of uncertainty of Optionality not materializing.

2.What would be the effect of Optionality not playing out on the existing state of the business?

Understand if failure of Optionality result in any adverse impact on the existing business of the company. Because if that is the case, then the Risk increases proportionately and should be compensated by an even higher reward.

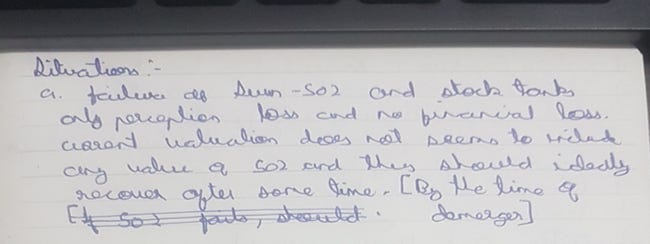

Back in 2019, the lead molecule of Suven’s Drug Discovery Business- SUVN-502 was in the late stage of Phase-II clinical trials, which if successful would have opened up an opportunity for Suven to license the same for further development for huge sums of money.

Given that Suven was just a ~3000 crores market cap company back then; the success of SUVN-502 would have been a game changer for Suven.

Now coming to risks associated with SUVN-502 Optionality.

1. Given that Suven as a company was being valued at just ~3000 crores, the market was not giving any value to the Drug discovery business. The market was not even valuing the core CRAMS business properly that was generating profits of ~100 crores even after paying for R&D costs of Drug Discovery and offered Non-Linear growth.

So, If SUVN-502 would have failed, which actually did happen, there should have been no major impact on the stock except for a very brief sentimental loss.

2. Further, it would have zero impact on Suven’s existing business, because Suven never took debt to fund its Drug Discovery, it was all funded by the CRAMS business. If Suven would have taken debt for the same, then it would have been a big problem, as the debt payment would have become a big drag on the company without the upfront monetization fee of SUVN-502. Moreover, all the money spent on R&D of drugs was always expensed in PnL and was never capitalized and thus there was no risk of a major write-off in the financials.

So the Risk:Reward in case of Suven was very favorable with entire Upside being open and a very cushioned downside.

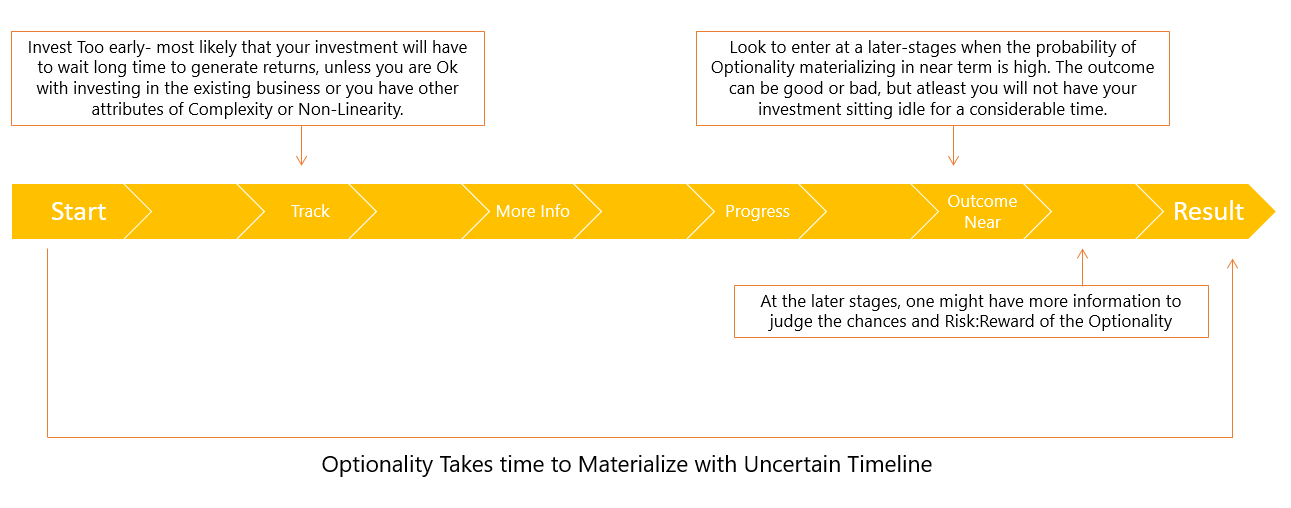

Timing Is Key In A Pure Optionality Bet

If you are looking at an investment to benefit from just a particular Optionality and not from other attributes like Complexity led value discovery or Non-Linear growth in Existing business, then timing becomes a key factor. And by timing I don’t mean timing the price of the stock, but the fundamental developments in the progress of Optionality.

In case of Suven, the other two attributes of Complexity and Non-Linearity were present and thus one could have invested anytime. But, if one wanted to bet primarily on the SUVN-502 optionality, then early-mid 2019 was the right time, as the Phase-II trial of the same was completed in mid-2019 and results were expected in later end of 2019, post which Suven would have looked to monetize the same.

Similarly, in case of JIO-Reliance example that I gave in the previous post; JIO optionality was under works for nearly 6 years from 2011 and materialized only in 2017. If one would have invested in Reliance much earlier than the investment would have sat idle as there was nothing much happening in the core Refining business. The test launch of JIO in the end of 2016 was a good fundamental development to invest in Reliance.

Keep an Eye on Key Corporate Actions

A lot of such opportunities play out when some key Corporate Actions take place-

1. First Concall

A concall is a very useful source in investing; you can pick tons of qualitative information based on what management is sharing, based on questions other investors are asking, which often gives alternate perspectives that you would have not thought about, It allows you to get a sense of management quality as well, based on how they are responding to questions; it also allows you to get a sense of market’s interest in the stock and finally the ability to ask questions and fill the missing pieces in your understanding of the company is very helpful.

Keeping track of companies that do a concall for the first time is very beneficial because it is the first time that a lot of qualitative aspects and hidden initiatives of the company can be known. This can allow us to capitalize on a possible opportunity early on and benefit from the value discovery that will happen once a larger part of the market becomes aware of the opportunity over time.

Markets wants spoon-feeding wherein everything should be clearly disclosed and visible. We talked about this in the previous post (click here) that Complexity / Lack of clear visibility makes it difficult for the market to estimate the true potential of the business and it is only when things are clearer the real value discovery happens.

2. Demerger/Closing/Sale of Business

Situations wherein a bad business unit is dragging the real prospects of a good business, as soon as the bad unit is closed or demerged, the real prospects of the good business is clear for everyone to see and that is exactly when the value discovery happens.

I earlier talked about how the Drug discovery business was a drag on Suven’s core CRAMS business and how the true profitability of CRAMS business was not clearly visible. This was going to change.

On demerger, every shareholder of Suven Lifesciences would have got shares in Suven Pharma and Suven Pharma would have very high profits. In FY19, Suven’s CRAMS business’s profit was ~180 crores; at ~3000 crores market cap, the company was available at 16x earnings (assuming Zero value of Drug Discovery Business), which was cheap.

Even after fact that Demerger will happen and that profitability post that would be very high for Suven Pharma due to no drag of Drug discovery business, market was still not giving any value to Suven. This is such a clear testament of what I discussed above, that a lot of times, market fails to discount true value unless the same is clearly laid out.

Just before Suven’s demerger completed in early 2020, the CRAMS business profits were ~270 crores and Suven’s Market cap was ~4000 crores, ie. the stock was even cheaper at just 14x earnings.

It is only when the company reported its 3rd quarter FY20 numbers, which was the 1st quarter post demerger wherein separate results were reported for Suven Life and Suven Pharma, that the market truly realized the value in Suven’s CRAMS business (Suven Pharma), because the reported numbers now clearly showed the high level of profitability of Suven’s CRAMS business. And then there was no looking back as with each subsequent quarter, the profitability of Suven became more clearer to the larger market and market even took cognizance of the strengths of the CRAMS business model. Even more, the Drug Discovery Business which was not given any value, now commands a market cap of ~1000 crores.

The chart below truly puts into picture how Suven saw large value creation-

Below is a snippet from my old Diary from mid-2019, wherein I wrote the basic thesis on Suven. Excuse the bad handwriting, never really had a good one 😅 .

So, this is all what I wanted to discuss on the framework of Investing In Complexity, Non-Linearity and Optionality. These are differentiated bets and truly deserves good allocation in an investor’s portfolio. One obviously cannot make entire portfolio from just such bets given that they aren’t many such investments. But try focusing on finding as many you can over your investing journey.

Summary-

Take the efforts to look where no one is looking and dig deeper and keep an eye on key events like Corporate actions.

Understand the Qualitative aspects and establish the strength of existing business.

Evaluate management to see if they can execute Non-Linearity and find & capitalize on Optionalities.

Evaluate the Risk:Reward

Be patient or get the ability to get in at the right time- this requires very sound understanding of the investment and also one should be able to appreciate what the price is telling you.

If you are reading this then Cheers to you, as you have taken the effort to read such a long post. 👍

Feel free to comment or reach out on Twitter for any further explanation or clarity. Have tried to balance the content depth and length, but there is always so much more.

Great insights into analytical part of the investing. I am new to this field and starting off a new self employment post my 34 years of service. Still a lot to learn and your articles like this are simple and easy to understand. I do realise the amount of effort it takes to create a document like this. My present comment is only to express my gratitude for sharing the knowledge. It is immensely helpful to newbies like us. Thanks a ton.🙏

Enjoyed reading the article. Copying a snippet from latest AR "But, when we received the information that our

SUVN-502 molecule did not meet the primary

end point, it was a painful setback. Because

our molecule was looked upon as a potential

blockbuster by most in the global pharma

innovator space. We knew it all along that it

was and will always be zero or one. Yet, it was

disappointing. After all, it was our first molecule,

and it had gone nearly the entire distance. "