Investing In Complexities, Non-Linearity and Optionality

Thoughts on a Differentiated Framework on Investing

There are multiple frameworks of Investing- Consistent Compounders, High Growth Investing, Investing in Small & Midcaps etc. each with its pros and cons, and these are pretty well discussed and practiced frameworks of Investing.

But one framework of Investing that is rarely discussed and is something that I really look up to is Investing in Stocks that are-

Little Complex to Understand

Offers Non-Linear Growth Opportunity

And may have Optionality

Such investments have the ability to deliver multifold returns not only because they can deliver strong earnings growth, but also because current valuations of these stocks do not sufficiently price the business’s future growth; and there are specific reasons as to why it is so.

Howard Marks : “Large amounts of money aren’t made by buying what everybody likes. They’re made by buying what everybody underestimates.”

But Let me first quickly highlight why value discovery is important in making multifold returns.

Now coming back to our primary discussion of why these stock’s deliver Multifold Returns.

Complexity

A popular school of thought in the market is to Invest in a Simple Idea, something you can explain a kid with a crayon. And if it is difficult than that, then it is probably a pass. I have a different thought to it,

Market can properly incorporate future possibilities of a simple, known, stable and easy to understand business. A business model that is something new, different and keeps evolving makes it relatively difficult for the market to incorporate its future potential in the valuations.

Complexity makes businesses difficult to understand & evaluate and thus they are largely under-researched.

Pharma as a sector can be a good example here, this sector continues to evolve over time creating newer business models on the back of innovations that allows companies to pivot themselves to something new. And each such new business model comes with its own set of complexities which are difficult for the market to dissect early on and thus allows investors to benefit from value discovery. Some examples-

First-to-File/Para IV Generics business model that evolved over 2010-2015.

CRAMS business model that has witnesses value discovery to an extent over last year.

Future value discoveries waiting to happen in the Biotech and New Drug Discovery business models that are still too complex for market.

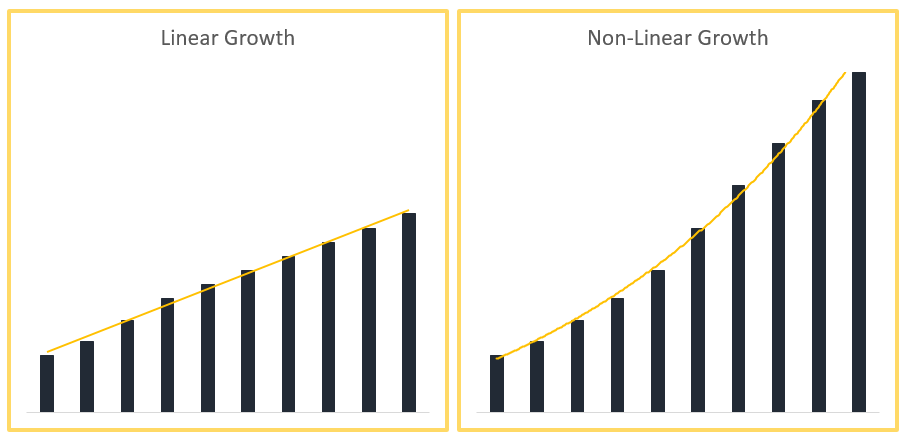

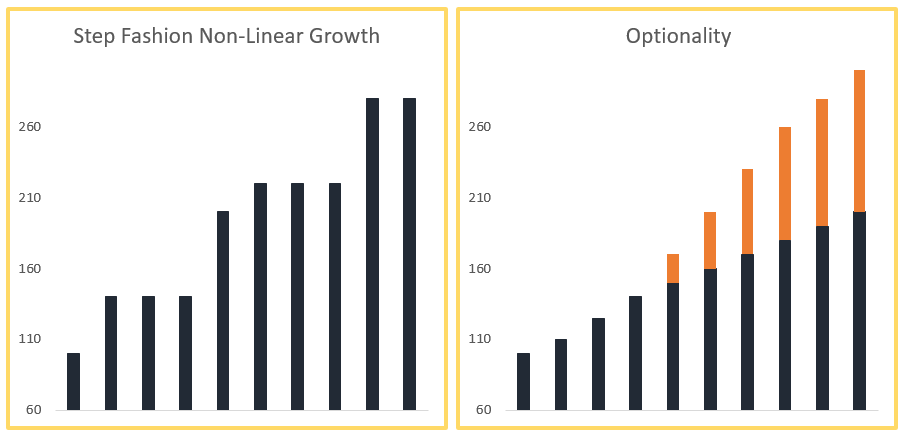

Non-Linear Opportunities and Optionality

Non-Linear Opportunities and Optionality in its true form allows a business to grow multi-fold in a relatively short period of time.

Possibility of Non-Linear growth depends primarily on a company’s business model and results from the dynamics of existing business. A business that gets incrementally better & becomes better with size can result in Non-Linear Growth.

Optionality on the other is something that currently does not contribute much or anything-at-all to the business, but it is something which is in works and if it is successful it can add substantial value to the company; like a

New Business

New Product/Service

Evolution of Business/Strategy

Investing in Optionality requires greater appreciation for of a company’s management and existing business strength, because timeline of an Optionality is relatively unknown.

However, there are always bits & pieces of possible future Optionality, which are available for everyone to see. All that is required is a better foresight of a business’s future potential.

New Business

This is pretty self-explanatory- JIO being a good example here,

Reliance started working on Jio is early 2010’s and till 2016 it was something which was under work and did not contribute anything to company’s business. But there were all kinds of information in Reliance’s Annual report to evaluate this optionality.

The optionality of JIO materialized in 2017 when it was launched commercially and now it is a substantial part of Reliance. Not to say that Reliance’s stock started moving after nearly 10 years at the very moment this Optionality got materialized.

One key pointer here is that if the new business is related to company’s existing business, then the possibility of such Optionality bearing fruits is higher as the company can leverage know-how and resources of existing business.

Some of the companies have also been able to convert their major operating costs into revenue generating businesses.

1) Classic example is Amazon that converted ever-growing computing requirements of its businesses into a scalable cloud-computing platform, which it later offered to other companies as a service- AWS (Amazon Web Services).

AWS now has $46 billion of annual revenues.

2) In India, IRCTC is one company that is trying to do something on similar lines by launching its own Payment Gateway- IRCTC iPay.

The cost for processing ticket payments which is done by payment gateways like PayU, Razor Pay, Paytm etc is charged to user and is a pass through for IRCTC.

These payment gateways charges from NIL on UPI & Rupay Debit cards to 0.4%-0.9% on Debit Cards and 1%-1.8% on Credit Cards.

But now with its own payment gateway, IRCTC can convert some of this pass-through cost as Revenues. And the opportunity is big, IRCTC processed payments of ~34,000 crores in FY20. Plus, IRCTC is also looking to offer this payment gateway to other government entities as well and generate revenues out of it.

New Product/Service

Here the optionality arises by expanding existing business into new products & services and increase value from existing business and customers. One good pointer here is looking for what more can be done for existing customers and fulfilling the same.

BSE comes out as an example here. BSE already being a platform providing investors with ability to invest in stocks added ability to invest in Mutual Funds with the launch of BSE Star Platform in 2009.

Star platform has been growing at a great pace with No. of Orders growing at 100% CAGR and Value of Order growing at 50% CAGR over last 5 years. This optionality is yet to play out fully given that BSE was able to generate revenues from the same starting FY18 only. In FY20 it contributed ~10% of BSE’s operating revenues.

But BSE is also looking to divest some stake in BSE Star and this would be the true materialization of this optionality as BSE would be able to unlock true value of BSE Star. One media article even quoted that Star platform is being valued at a massive Rs2000 crores; BSE’s entire market cap is just ~2500 crores.

Even though I don’t think that the valuation would be that high, but it would be a substantial value creation for the company.

Evolution of Business/Strategy

This Optionality plays out when a company’s existing business evolves or pivots to a better version of itself. Such pivot allows a company to increase its growth, secure market leadership, increase profitability, increase scalability of business etc. Basically, the way a business is done is changed.

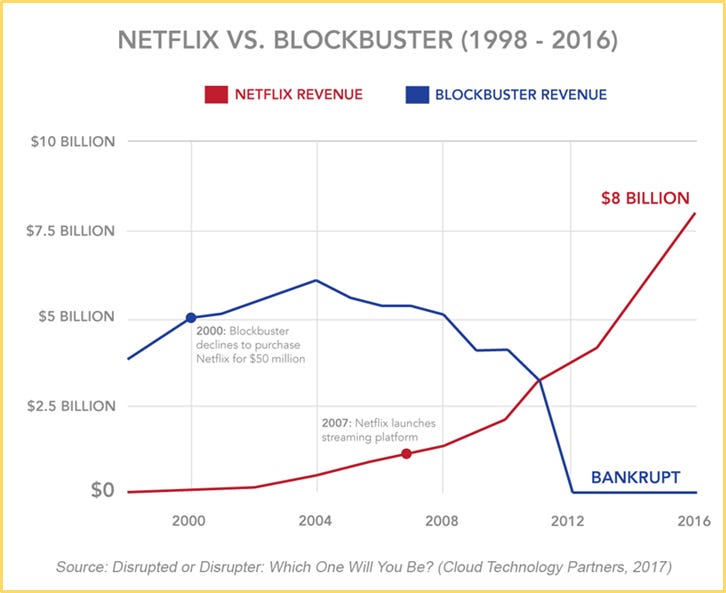

Such optionality is very rare and there are very few examples of such Optionality. One of most quoted example of successful business pivot is that of Netflix.

Netflix initially started as a DVD rental company. They used to compete with Blockbuster which was the market leader in DVD rental. Even though Netflix was fast gaining market from Blockbuster as it had a better business model being an online only company; it used to send DVDs through post, whereas Blockbuster was primarily doing the same through physical stores and added online store at a later stage. Netflix was still the 2nd player and much smaller than Blockbuster.

But the pivot happened in 2007 when Netflix started offering online streaming of movies as they sensed the growing popularity of Youtube and Internet Streaming. This changed the way people consumed entertainment at home. This evolution of business strategy allowed Netflix to cement its dominance in the home entertainment industry while Blockbuster, who failed to pivot went bankrupt in 2012 as DVD sales topped in 2007.

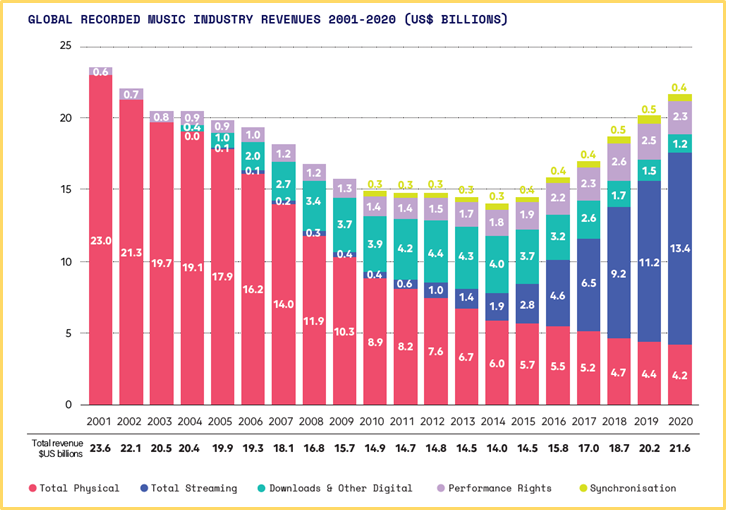

In Indian context, one industry that is going through the same kind of evolution of business is the Music Industry and this is part of a global shift in the music industry.

Globally, the revenues of music industry topped in 2000 as growing internet adoption gave way for all kinds of piracy and sales of music disc, cassettes etc fell. The business model here was never really able to evolve. But that has changed in last few years on the back of Streaming services like Spotify, Apple Music, Gaana etc.

I don’t think anyone now download songs, most people use either Youtube or Spotify etc. These streaming services have been able to generate revenues from music listeners either through subscription fees or advertisements. And a part of this revenue is now flowing to Music companies.

Two listed companies in India- TIPS Industries and Saregama are witnessing the benefits of the same. Both of them have licensed their music catalogue to all streaming players like Youtube, Spotify, Apple Music, Saavan etc. And are seeing strong growth in Music License Revenues. 2/3rd of Indian Music Industry revenue is now coming on the back of such Streaming Platforms.

Music License Revenues..

Even if someone is able get a good understanding of such Complex business and is able to identify Non-linearity & Optionality, I have seen that people rarely Invest in such stocks because of the Perceived Risk.

To summarize, the combined factors of the business being little complex to understand or analyze and the perceived risk, these are typically under-researched and less tracked companies, which directly results in underappreciation of future value in such names.

I believe that such kind of bets deserves a place in an investor’s portfolio. Market is relatively efficient in valuing known business, but it struggles to value the less knowable.

You might not get all the three attributes- Complexity, Non-Linearity and Optionality in an Investment. But even 1 or 2 of these can help generate strong returns.

I was going to add few points on How to Find & Evaluate such Opportunities, but given that this post has already got extended, I’ll explain those points in a 2nd post (Click Here) with a very good example of an investment that had all the three attributes- Complexity, Non-Linearity and Optionality.

A very simple note on complexity. Brilliant.

this is a great post, keep up the good work