Journal #2- 21/06/21

Snippet, Good Reads, Stock Insights-NIRLON and Portfolio

Journal is a recurring series of posts wherein I look to share parts of my day-to-day activities around Full-Time Investing like Notes, Resources, Learnings, Insights and Portfolio Updates. (Previous Journal)

Snippet

There is a saying in the market that one learns from their experience; which is true atleast on the individual level. But having experienced a past mistake does not necessarily means that one will not repeat the same.

The true reason why we have excesses in the market- both Boom & Busts is because market as a whole fails to remember how the last one ended; this is most popularly termed as “This Time Is Different”.

But every boom & bust is the same in the sense that they are driven by excessive greed & fear. The only thing that changes is that, which is what the above snippet highlights, is that, when you are part of such boom & bust, it is extremely difficult to realize such excess greed & fear.

Good Reads

This is another deep insight from Morgan Housel wherein he brings to light a practically applicable idea that most things in life cannot be a Yes or No or say 0 or 1.

The best part of each thing in life lies somewhere in between these Yes/No or 0/1- The Optimal Level.

He lays out a very good example as well that, in a grocery store one can look to eliminate theft by strip-searching every customer leaving the store. But that would also mean that no one would want to shop at a grocery store that strip-searches everyone. So, theft can never be zero. One has to accept a certain level of theft as a part of business.

Similarly in Investing, there is no investment/company/stock which is perfect- something that will check all the boxes of your checklist. One always needs to accept some Ifs & Buts in a stock, but that also does not mean that one would allow all sorts of Ifs & Buts. There has to be an Optimal level for the same.

In one of the earlier posts (Click Here) I had talked about balancing this threshold of allowing such Ifs & Buts in Investing.

The article details how one of strategies used in Chess called Seizing The Middle can be applied to areas of Business, economics and negotiations. The strategy basically involves using pieces to dominate the middle of the board so that one can then restrict their opponent’s movements by controlling the maximum number of pieces in the game.

The post details how John D. Rockefeller used the strategy to dominate the Oil Industry and become the richest men. He basically went out to control one of the core pieces of the oil industry- Rail Roads, which restricted the ability of the competition to freely move oil in the United States in a competitive manner.

The more I thought about this strategy and reflected on the same, I realized that some of the most successful companies of the 21st century have adopted the same strategy. Apple is the finest example here. By maintaining a closed ecosystem of software and hardware, Apple has been able to restrict any other company to make money of its ecosystem of hardware, users and software. In one of the recent moves, Apple has restricted the ability of Advertisement players like Facebook to effectively monetize it’s users data. This is on the back of Apple’s push to get big time into Ad space by monetizing it own Software Ecosystem.

Stock Insights

Nirlon is among the select few companies like those of Nesco and Phoenix Mills, that have pivoted from a legacy business to a Commercial Real Estate business. All these three companies have successfully monetized the land bank of legacy businesses in the land starved city of Mumbai, by offering commercial assets like Malls, IT Parks, Exhibition Centers etc at prime locations in Mumbai.

Phoenix Mills used the old Textile mill location to build the iconic High Street Phoenix & Palladium Mall at Lower Parel while Nesco used the old engineering business land at Goregaon to build Exhibition centers and IT Parks.

Commercial Real Estate is a great business if you have prime land bank. You get annuity income that grows 12-15% every 3 years (in case of Office space, for retail assets like Malls, it could be higher) as rent escalations are built into lease contract. Plus, once a lease expires, the new contract can come at a substantially higher rent depending on the market scenario. These companies can then reinvest the cashflows into building more assets which when commercialized gives a good step-fashion growth.

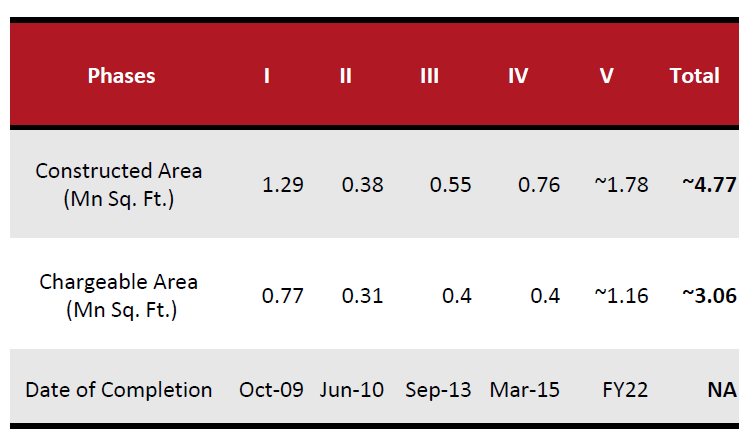

NIRLON was earlier into Textiles and later used its prime land situated in Goregaon to build IT Parks. Nirlon owns ~23-acre land near Western Express Highway in Mumbai; just slightly ahead of Nesco Center. The development of this land into an IT Park started in 2006 in phases. Till date, company has developed 4 phases totaling a leasable area of 1.9 million sqft. The final phase- Phase 5 is expected to be completed this year.

The thing that got me interested here is that the new Phase-5 is going to add ~1.16 million sqft of leasable area which is about 60% increase in company’s existing leasable area. So, it is going to be a big jump in total leasable area. Further, an even more exciting fact is that the company has already leased out this entire new Phase-5 to JP Morgan.

As per the company, Phase-5 will add ~200 crores annually to revenues beginning from Q4FY22. Nirlon’s FY20 revenues were ~300 crores.

Another good part here is that Nirlon is owned ~64% by GIC Singapore- GIC is Singapore’s sovereign wealth fund and GIC has extensive experience in real estate investments in India.

Further, nearly a 1 million sqft (33%) of leasable area is coming up for renewal in next 3 years.

So, business wise things are looking great here. The only thing that is left is to understand what valuation will market give to Nirlon.

Typically, a commercial real estate business is valued based on a cap rate, that is applied to Net Operating Income. A lower cap rate means higher valuations. In India, typical cap rates vary from 7-9% and is dependent on various factors like,

1. Type & Location of Property- As the saying goes, in case of real estate, it is all about location, location and location. In terms of location, Nirlon is well placed as it has a prime location in Mumbai. Retail assets like Malls get higher valuations and thus lower cap rates, while office spaces get slightly higher cap rates.

2. Growth Prospectus- This is where Nirlon is at a disadvantage given that post Phase-5, company does not have any more land to develop. The only growth that would come, would come from rent escalations every 3 years and renewal of leases at higher rates.

But I do have a gut feel that GIC would have some plans to use the increased cashflows of the company apart from servicing the debt. Company has recently hired an investor relations agency as well and will be holding its 1st concall this week.

Nirlon would end FY21 with ~320 crores of revenues; adding Rs200 crores of revenues that are expected from Phase-5 we get Rs520 crores of revenues. Company makes 75-76% of revenues as operating profits, so that would be roughly 400 crores of Operating profits- post tax Rs300 crores. At 9% cap rate, Nirlon would be valued at ~3300 crores (300/9%). Do note that the valuation based on cap rate is the value of the company including debt. Nirlon has ~1000 crores of debt that it has taken for various phases of development. So, equity value would be 2300 crores. This entire debt would get repaid in a couple of years as Nirlon would generate nearly 500 crores of free cash annually. Since markets are forward looking, there is good possibility that the debt part would not be considered in Nirlon’s valuation.

Nirlon currently trades at a valuation of ~2600 crores. My thoughts here is that the downside looks well protected even at high cap rate and upside possibility depends on how well & quickly the market values 500 crores plus annuity cashflows. The stock here has been flat since GIC’s acquisition in FY15 and has only recently started moving. And when it comes to valuations, the price is the best leading indicator according to me.

Something to keep an eye on!

Portfolio Updates

CORE PORTFOLIO

No Change & No Update

TRENDZ PORTFOLIO

No Change & No Update

That’s All For This One

21/06/2021

Wouldn't Nesco be a better bet, considering that they too are in the process of setting up another IT tower. Plus they have plenty more land to pursue similar developments in the future. Although the management may not be as great as GIC Singapore. Look forward to your views.

Do you see 3 years down the line,Nirlon giving 50% of cash flow as dividend which would be in the range of 30 Rs.