Journal #3- 10/07/21

Snippet, Good Reads, and Portfolio Updates & Performance

Journal is a recurring series of posts wherein I look to share parts of my day-to-day activities around Full-Time Investing like Notes, Resources, Learnings, Insights and Portfolio Updates. (Previous Journal)

Snippet

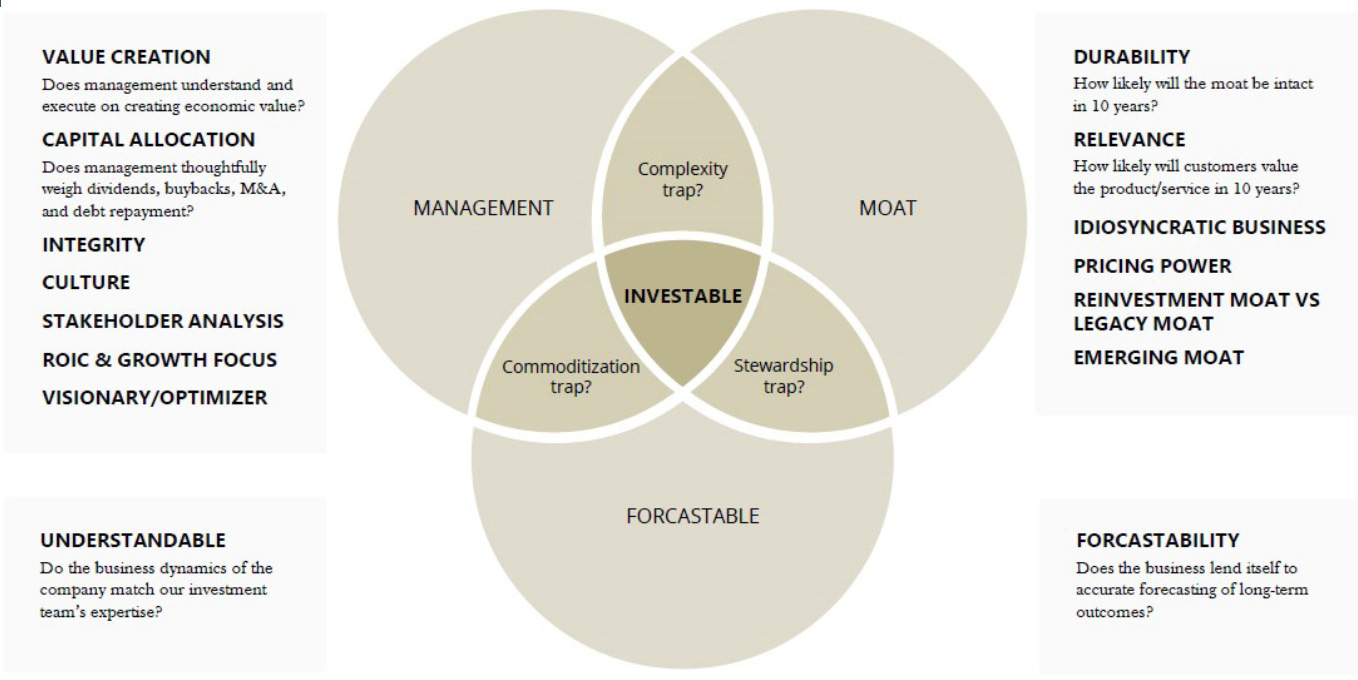

The above image broadly highlights the stock selection framework of Ensemble Capital. There are three core pillars that makes up the framework- Management, Moat and Forecastable. The first two pillars- Management and Moat is something that a lot of people talk about, but what caught my attention was the pillar of Forecastability, which is not much talked about.

Sean Stannard-Stockton (CIO of Ensemble Capital) describes that the pillar of Forecastability should be seen not just from our point of view as to whether we can forecast the business (i.e The Circle of Competence), but also from the business point of view, as to whether business is such that it can be forecasted in a reasonable manner in the long run.

And what he says is true, some businesses are inherently more forecastable than other businesses. And we don’t have to compare something with a cyclical commodity business to understand this, even if we take two companies like Nestle and Maruti (Both Leading Consumer Brands), an FMCG business is more forecastable than an Automobiles business.

In my Game Of Stocks post, I had shared that my primary focus is on Niche, Unique & Differentiated businesses wherein the business model itself is so strong that it can deliver sustainable & profitable growth. And such strong business models also allow for a better forecast ability if the same is within your circle of competence; at-least on the profitability side it does for sure.

Good Reads

1. The One Percent Show- Vinod Sethi

This is one of those reads wherein you literally spend hours reflecting on ideas that you come across. Mr. Sethi has shared great insights from his vast experience across life and markets.

I am highlighting here some of key insights from the market’s perspective-

Soros- “Buy when there’s no one left to buy”. This is an extreme version of Warren Buffets famous quote- “Be greedy when others are fearful”. Mr. Sethi shares the story of how he used this principle of Soros to buy 15% of Tata Motor’s GDR issue in early nineties when were no other subscribers to the issue.

Inner explosion or the inner Nirvana happens when you’ve caught what was on its back. If I have a high conviction and capital, I’d like to be the first one in; I don’t like to get into the highway midway. A Hero Honda, HDFC, Tata Motors interest me deeply, but If you asked me to buy HDFC at 40x earnings, that doesn’t interest me, even if have the conviction and capital.

Commonalities of Potential Wealth Creators- Inherent Capital Productivity of the business (ROCE/ROIC) + The way the business is run (Management).

There’s merit in the view that prices drive fundamentals- I would always urge caution that delusion is a self-feeding loop because when something is a hundred-times earnings it, you think it's good. And because it's good, you think it's at hundred-times earnings.

I remember meeting the head of ACC when the stock was almost at nothing, at around Rs 100. As soon as I entered the room he said, “Why have you come? There's no future. This industry is down the toilet. There's nothing here.” I met him again when the price was around Rs 10,000. Same person, same office, same building. He tells me ACC was the best story in the world and that it was the cheapest stock you could find.This one is quite practical- The market is not waiting for you to complete your homework for the prices to go up or down. One has to act when the prices are going up or down and not when one has completed the work. Just because you have spent a hundred hours on something, you don’t need to act. The key to being a good money manager is to not act or not link your work with your action. Delink the two. One has to keep working, the conviction and intuition will come over time.

Explained with a great analogy-

2. MeWork

This post is a great mix of humor and practicality. The post talks about the idea of a new age of CEOs/Managers/ entrepreneurs called as MeWork generation (most likely named after WeWork fiasco). The MeWork generation basically makes their fortunes by losing money.

The author has devised two metrics to measure the MeWork generation- Daily Benjamin Burn (DBB) and Earn-to-Burn Ratio (EBR).

DBB is basically how much money the MeWork executive has lost on a daily basis while he/she was running the show and EBR is basically how much money the executive has made while losing that money- think of it as a commission for burning money.

Author provides many examples of such MeWork generation with their DBB and EBR. The best example is obviously that of Adam Neumann & WeWork.

In India we can try to measure these metrics for say a Zomato. Over last 3 years, Zomato has lost >Rs4000 crores. This translates to a Daily Benjamin Burn of ~3.8 crores. Earn-to-Burn Ratio would be hard to establish given that Deepinder Goyal’s earnings from Zomato is not readily available. But as per Zomato’s RHP, Deepinder will get Rs3.5 crores annually as basic pay, other benefits like Variable pay, ESOPs etc would be extra and a large sum. On the basic pay alone, the EBR here would be ~0.25% [(3.5/365)/3.8]

Portfolio Updates

CORE PORTFOLIO

Added Gland Pharma in the Core Portfolio

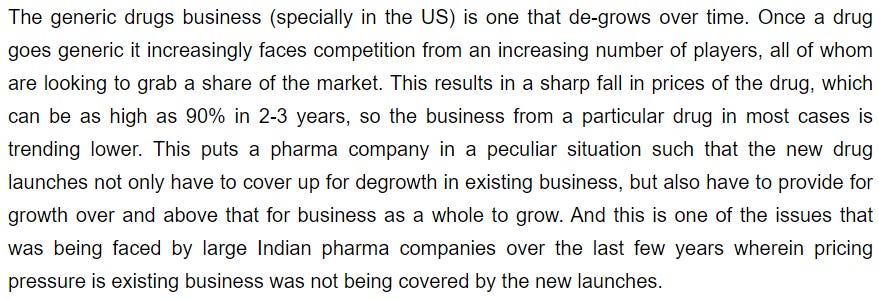

Gland is another company with extremely strong business model that allows for sustainable & profitable growth. Gland’s business model addresses the biggest pain point in a generic pharma business.

In my Natco Pharma blog, I had highlighted a major issue faced by generic pharma companies-

Gland’s business model is such that it is able to not only sustain its existing business but is also able to grow it (base business grows by low single digits as per management). The way Gland is able to achieve this is by working under a transfer pricing model (plus some profit share). In Natco’s blog I had highlighted how typical arrangements happen in pharma-

Instead of working under large pure profit-sharing agreements, Gland largely works under a transfer pricing model wherein Gland supplies the product to its partners on a cost + profit margin basis, plus a small profit sharing. What this does is that when the price of drug falls and profits of the partner reduces, Gland’s profits are not affected by large extent given that its profit share is small. The profitability from the transfer pricing is not affected from the erosion in drug’s prices as that is restricted only to profit share component, which is small for Gland compared to other pharma companies wherein entire profits are a result of profit-sharing component.

As per Gland’s management, the gross margins for new launches in 65-70% which then reduces to 50-55% in 2-years or so. This indicates that the price erosion that happens in the initial 2-3 years has a smaller impact to Gland’s profitability as profit share captures only a small part of Gland’s profitability.

Further, Gland’s business model is that of a contract manufacturer and it does manufacture the same drug for multiple marketing partners. This basically allows Gland to capture incremental volumes for a particular drug over time.

So, a combination of less impact of price erosion in drug prices and increasing volume share results in a situation wherein the existing products also contributes to some growth and new launches does not has to compensate for any degrowth in existing business.

Also, Gland works purely in the injectable drugs space. Injectables relatively is a less competitive part of pharma as injectables are difficult to manufacture, get approvals for and maintain quality. Even a company like Natco only manufactures the API (raw material) for its flagship product Copaxone. The final drug is manufactured by Gland for Natco. This is because setting up & maintaining a manufacturing infrastructure for injectables is very expensive.

In totality, Gland has a very strong business model in an industry where the opportunity size is quite large and there is scope for multiple pivots. There are quite a lot of interesting things here, I’ll look to cover more details though a separate post.

Removed HAWKINS from the Core Portfolio

My original rational on Hawkins was that of a consistent compounder trading at valuations that are relatively lower compared to other consistent compounders with similar metrics and I had expected a re-rating. Plus, a breakout to new highs after 5 years also hinted that market dynamics are in favor (Understand the role of Market Dynamics). Hawkins stock continues to trend upwards and I do expect that the original thesis will play out, with it being only a matter of time.

However, I always prefer investments wherein the rational is primarily on earnings growth rather than on valuation re-rating; because valuations are largely dependent on market dynamics. And this is why I have chosen to exit Hawkins to make space for Gland in the portfolio.

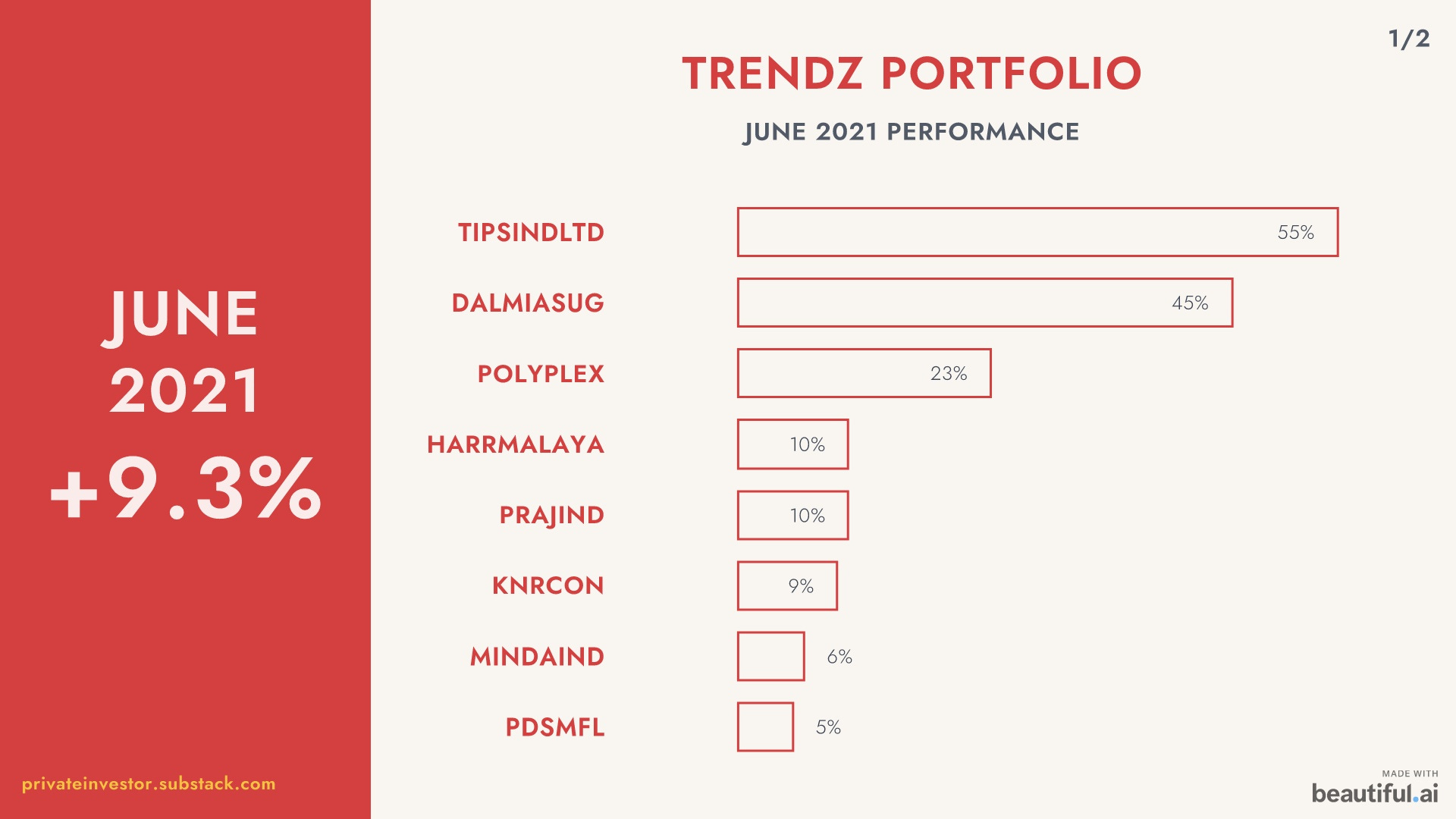

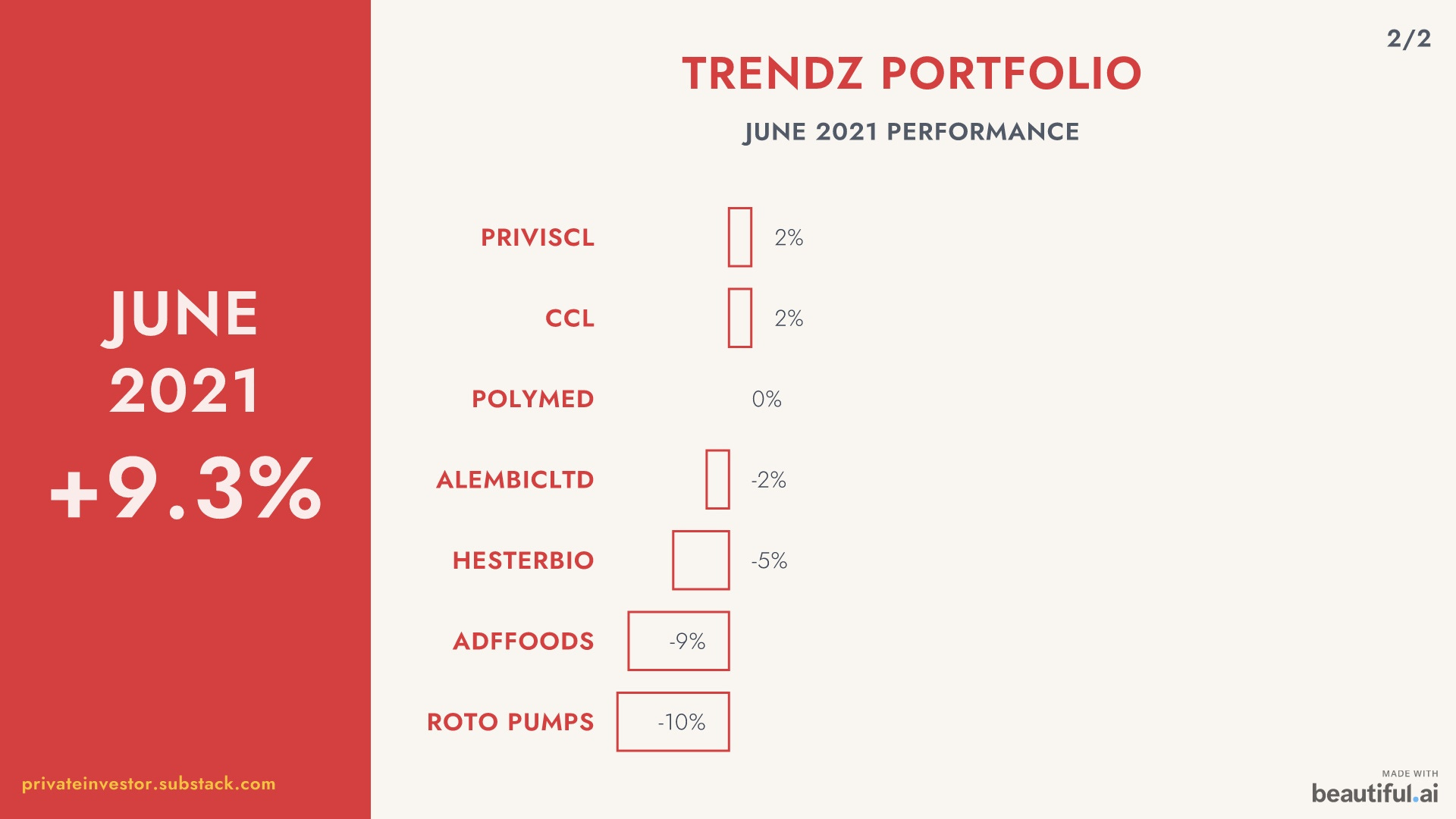

TRENDZ PORTFOLIO

No Change

That’s All For This One

10/07/2021

Why don't other companies undercut Gland's (cost+profit margin+profit share) model especially when they enjoy such high margins? Does Gland deal in products where competition doesn't exist?

Also, isn't Gland expensive currently? I feel all ratios stop me from purchasing it, high PE, high PB, high Price/Sales, low CFO/EBITDA. Wanted to know your opinion on valuations given it leaves very less margin of safety compared to other opportunities present in the pharma industry.

PS: Love your Journal & insights. Thank you for the content.