Journal #4- 19/08/21

Journal #4- 19/08/21

Snippet, Good Reads, and Portfolio Updates & Performance

Journal is a recurring series of posts wherein I look to share parts of my day-to-day activities around Full-Time Investing like Notes, Resources, Learnings, Insights and Portfolio Updates. (Previous Journal)

Snippet

Above snippet highlights the best market environment for a company to be in. It broadly talks about the 3-layers of market environment-

1. The overall Size of the Market- If a company is into a business wherein the end market opportunity is currently very small and growing fast with potential to end up becoming a very large market then a company has a very conducive environment to flex itself.

2. The formal Pie of the Market- If the market structure is such that the unorganized players still hold a large part of the market then you have a double kicker of growth as growth in size of the market translates to an even faster growth for the organized player as market share shifts from unorganized players.

3. Inefficient Part of the Market- If within the organized share of market you have a situation wherein there are Inefficient players that are losing market share, then it acts as a third kicker for growth.

In such a market environment an organized-efficient player can have a very high growth that is a cumulation of-

= Industry Growth

+ Additional Growth from Growing Share of Organized Players

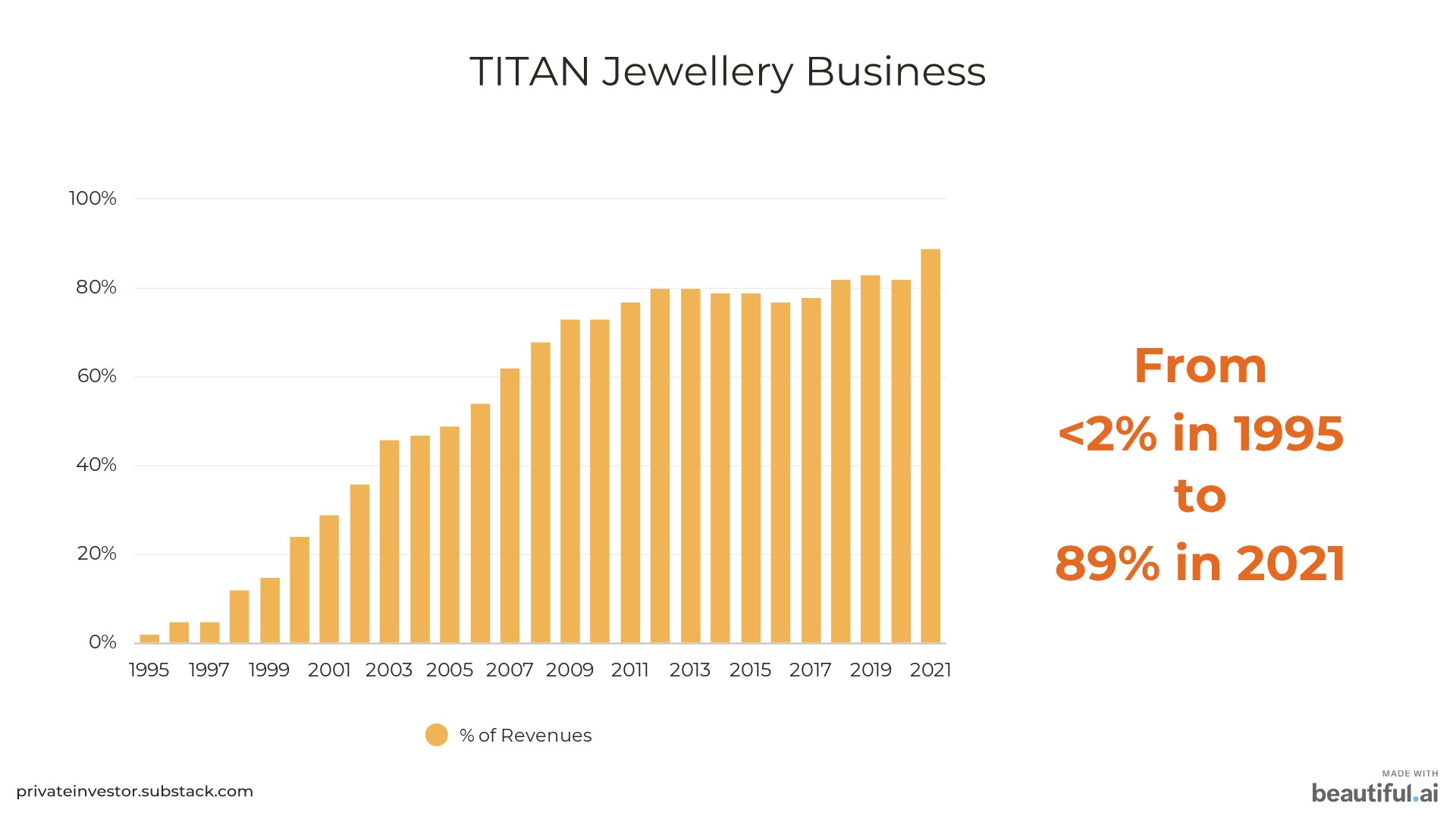

+ Additional Growth from Inefficient Players Losing Market ShareBut such market environments are extremely rare. Titan is one company that has benefited from such a market environment in its Jewellery business.

Just look at the sheer growth that Titan has enjoyed and continues to enjoy because of it. Titan has recently launched Taneira which is into Sarees and kind of enjoys similar market environment.

Power Exchange business is another example wherein the market environment does offer such 3-tier growth potential in the sense that,

1. There is growing power demand in India with enough room to grow multifold

2. Share of Short-Term Market in overall power market has potential to grow from current ~10% to ~40-50%

3. Share of Exchanges within the Short-Term power market continues to grow by taking up more & more market share from inefficient avenues of traders & bilateral contracts.

I had earlier written about Power Exchange business in detail-

Good Reads

1.Hayden Capital Q2 2021 Letter

This latest letter from Fred Liu is the best resource to understand the true reason behind recent crackdown by China on its Tech giants. The letter provides some good insights on difference in Chinese policies and that of other developed countries in West, specifically around use of Capital.

Liu provides historical reference that when China was opening up in 1980s, Deng Xiaoping (former leader of China) famously said “Let others get rich first”. The idea behind this thought was to allow certain section of society generate large wealth and then use that capital as a tool to enhance & accelerate society’s goals.

The intention of this policy was not to allow some to get rich and then use this capital to then go squeeze even more profits from the weaker sections.

This Liu highlights is stark opposite of wester countries wherein end goal of capital is that of betterment of shareholders and putting more money in the hands of select few.

The letter also talks about why Education sector is worst affected by the same. China has been witnessing widening income gap and the one of the best ways to fix the same has been through better education. Liu talks about importance of China’s Gaokao (college entrance exam) and growing financial & other pressure on its citizens due to the same. And that China’s recent actions are primarily directed towards fixing this.

And I think Fred Liu hit the head on the nail with his thoughts. In last 20 years, China has let select tech companies amass large power as it supported overall society and ecosystem to develop. But now once that stage is done, China now wants to put a tight leash on these tech superpowers and wealthy people like Jack Ma, who has gained significant capital in process, to now use that capital and resources for societal goals.

One important learning that Fred shares in the letter is that if one wants to invest in foreign countries, first they need to understand the history, culture and context of its people first. And this is especially important for countries like China wherein the government has larger control over different aspects.

2. Learnings from Polen Capital

This post contains notes from a recent interview of Polen Capital’s Dan Davidowitz and Jeff Mueller. Dan and Jeff have shared their quite interesting perspective on some of investing topics.

A. On Compounders-

Just because a company has high ROCE & ROE does not mean that it is a compounder.

It is the sustainability of this high ROCE & ROE that makes a company a compounder.

The necessary condition for sustained high ROCE & ROE is a competitive advantage.

Understanding competitive advantage requires critical thought and judgement and one cannot just run a screen and buy stocks

Compounders are often found in areas of low total addressable market penetration, ideally in a very large total addressable market and even more ideally, in one that is growing. This is something we have discussed in the Snippet above.

B. On Value-

In brief their thought is that the old way of value was to buy something at a fraction of its Present Intrinsic value. But the new way is to buy something at a fraction of its Future Intrinsic value even if it entails buying the same at its Present Intrinsic value; a.k.a-Growth Investing.

C. On Competitive Advantage-

There is a theory that you can’t truly know the moat or barriers to entry exist until that moat is attacked and the attack is repelled.

D. Perfection-

You can study and study companies but you’re never going to know everything you’d like to know.

You’re going to know a fraction of what an insider knows and they don’t know everything either.

You have to be careful because you’re never going to know everything.

Portfolio Updates

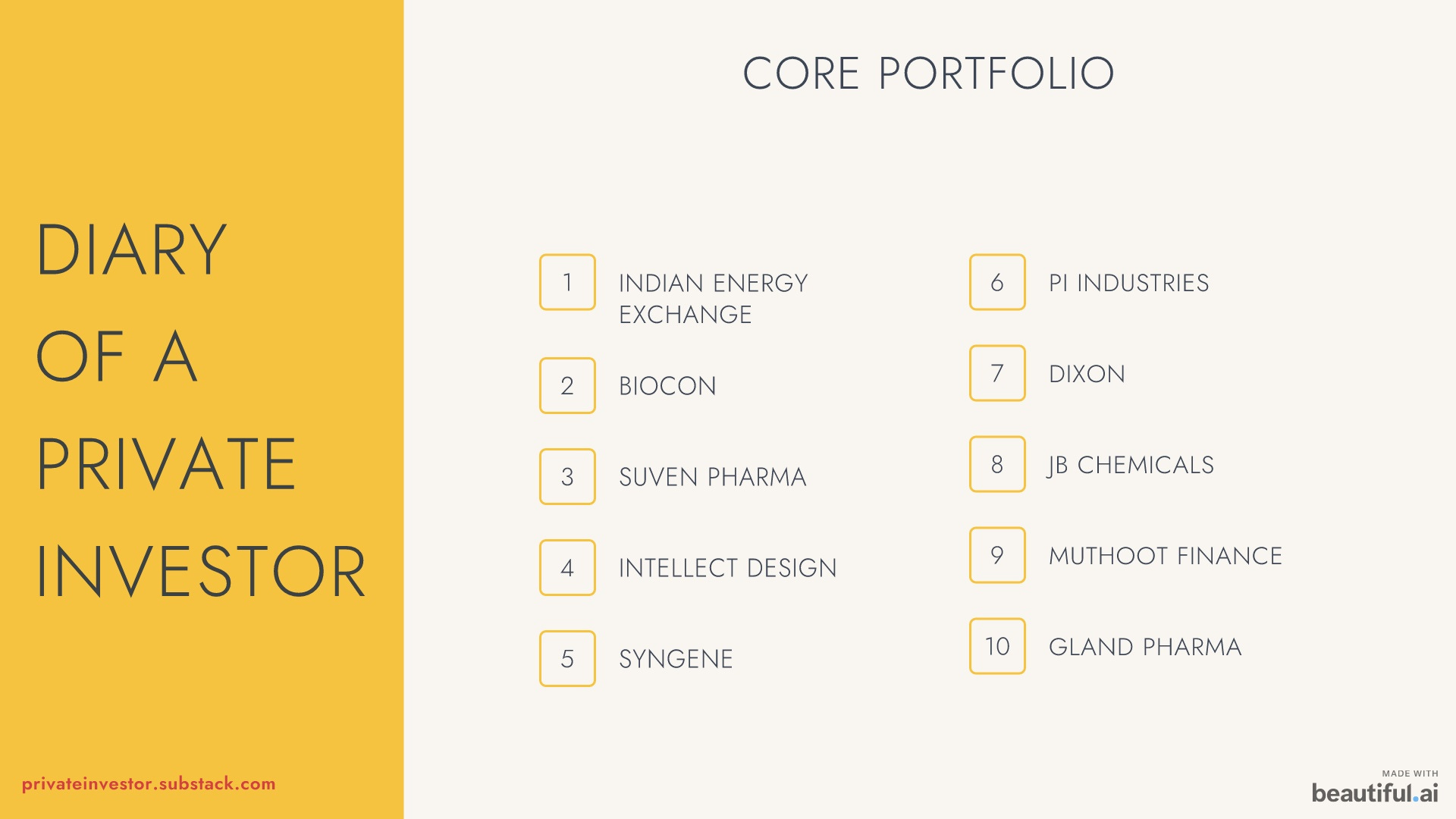

CORE PORTFOLIO

Exited InfoEdge

In my Game Of Stocks post, wherein I had shared small rational on each CORE Portfolio stocks; I had mentioned that I am looking to exit InfoEdge in near term.

My original thesis when I bought InfoEdge in 2019 at ~2000 level was that growing valuations of new age tech companies and public market’s growing interest in such companies could lead to Infoedge becoming a primary beneficiary of liquidity chasing such companies.

In recent times It came to a point that some of the investments of InfoEdge were looking to go public and I had expected this to be another leg of value unlocking for InfoEdge given that IPOs would come at substantially higher valuation levels. At the same time, I became cognizant that this would be the final trigger for InfoEdge because post these IPOs the liquidity will no longer favor InfoEdge as many such new age tech companies had announced their IPOs and thus liquidity would move to such companies. And this became quite evident on listing on Zomato when even though Zomato doubled on listing, the price of InfoEdge did not budge a little even though InfoEdge owns a significant stake in Zomato.

And as a result of no more future triggers in sight, I exited the same on the day of Zomato’s listing.

I have used the cash from InfoEdge to increase allocations in recent additions of Muthoot Finance and Gland Pharma.

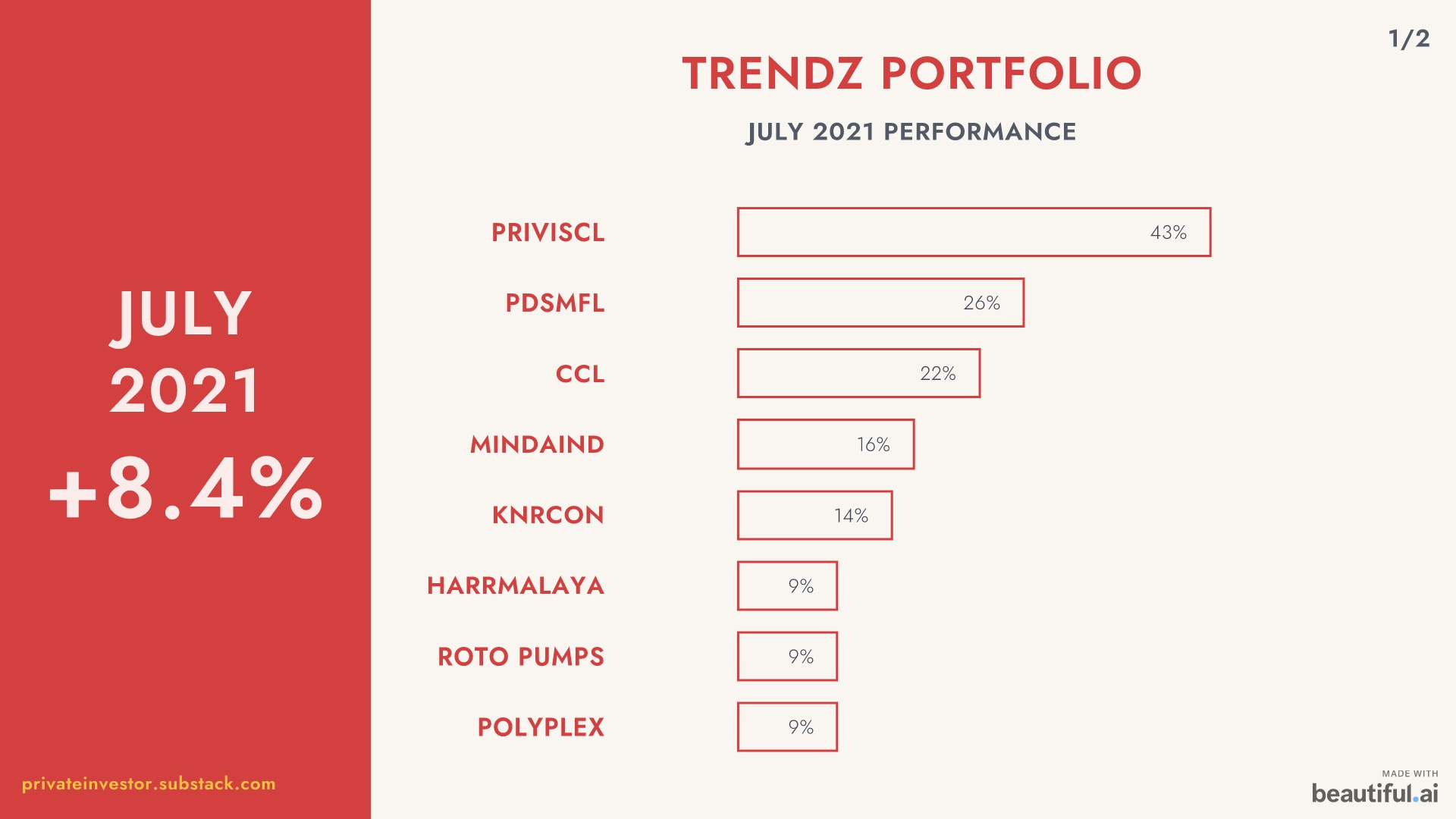

TRENDZ PORTFOLIO

No Change

That’s All For This One

19/08/2021

I liked the content...quite appropriate & nicely put.

Very Good Insights, with some interesting reads , what would be some Top PMS whose letters you follow regularly