Journal #5- 02/11/21

Journal #5- 02/11/21

Snippet, Good Reads, and Portfolio Updates & Performance

Journal is a recurring series of posts wherein I look to share parts of my day-to-day activities around Full-Time Investing like Notes, Resources, Learnings, Insights and Portfolio Updates.

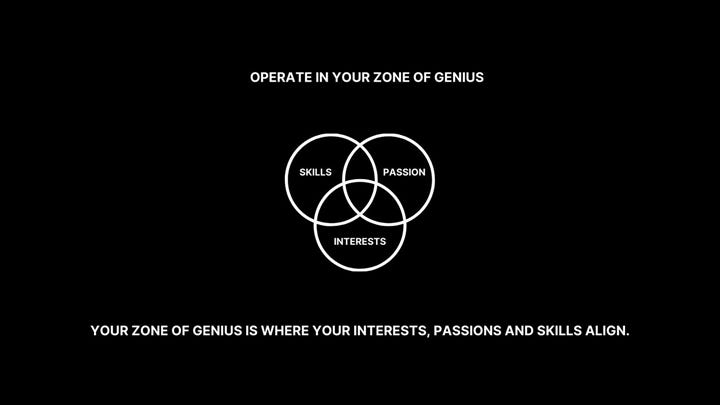

Snippet

Above Snippet is a great hack on how to approach the Work aspect of your Life and is something that can be applied to one’s approach towards equity markets.

Everyone knows that there are hundreds of ways to make money in the markets. One can do intraday-trading, FnO, Scalping, Value Investing, growth investing, momentum investing, trend following, algos, passive investing and many others. But one can never succeed in all these ways or even in multiple of these, one has to figure out what works for him/her and only then can one succeed in the market.

And the framework highlighted in above Snippet is a good hack to figure that out.

It is basically the concept of Circle of Competence on STEROIDS!

1. Figure out if you are passionate about markets.

Two things to keep in mind when evaluating this-

Markets are volatile, Hyper competitive and always changing.

“Stock markets is the easiest business to do, but the most difficult one to make money in”

2. Identify if your Skillset is more suitable for Trading or Investing.

Trading requires skills around faster decision making and better emotional balance.

Investing requires patience and ability to read, read & read.

3. Finally determine what Interests you.

Like in Investing, do you like growing business and evaluating future possibilities in a business? Or you are more into finding market inefficiencies and want to benefit from value unlocking?

Once you have narrowed down these three areas, you have your moment of FLASH OF GENIUS.

Good Reads

1.This Is Why We Need Fiat Money

This is the best argument that I have read against something like Bitcoin taking over as the new form of currency. This is a must read for everyone. (Small 5min Read)

Amazon has recently launched a multi-player online role-playing game called New World. In this game, the amount of currency is limited, something like how Bitcoin is limited to 21 Million. Overtime as more and more player joined the game, the demand for money increased and with a limited supply, the value of money started rising.

This resulted in a situation wherein existing players with money started hording it resulting in an even lower supply and thus more increase in price. Further, more & more players started offering goods & services in order to get hands on money, resulting in a situation wherein supply of goods & services increased while people willing to spend money decreased, resulting in massive deflation.

This went to a situation wherein players had to resort to barter system as there was no money to exchange goods & services.

This, the article highlights is a good example of what would happen if we went back to a gold standard or adopted cryptocurrencies as legal tender. In real world, demand for money has to grow as the population grows.

In my recent post on Intellect, I had talked about how Buybacks can supercharge returns for investors with some examples of Autozone and Visa.

But the most fascinating example of Buybacks and effective use of Stock is that of Henry Singleton and Teledyne.

Over 1965-1970, Henry Singleton used Teledyne stock to acquire 130 companies as its stock was trading at rich valuations of 40-70x earnings. Over this period the no. of shares went up 4x.

Then in 1970s as the market went into downturn and Teledyne’s valuation collapsed to 10x earnings, Henry started buying back stock from open market so much so that the number of shares reduced by 90% over 1972-1984.

The net effect of buyback was that the price of Teledyne’s stock went up by 30x over this period of buybacks.

Portfolio Updates-

It’s been a long time since I wrote the last edition of Journal and there has been a couple of changes in both Core & Trendz portfolio. I had posted updates around Trendz portfolio on Twitter on regular basis, but for Core Portfolio, I didn’t do that as I wanted to provide rational alongside.

But Apologies for the lag in update.

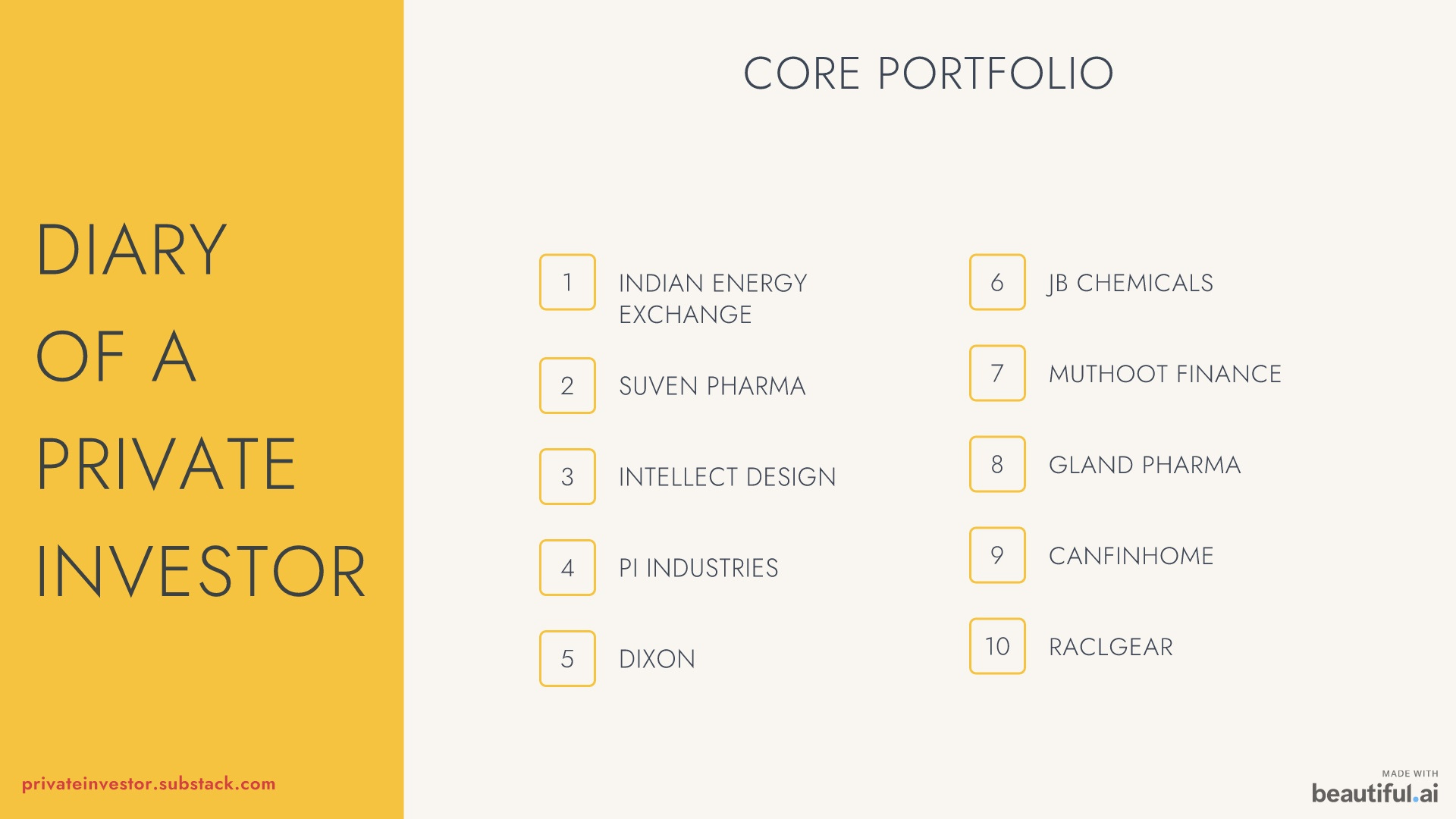

CORE PORTFOLIO

Exited- Biocon and Syngene

Added- Canfin Homes and RACL Geartech

Biocon-

My thesis on Biocon was on the potential of its biosimilars business. Biocon has been at the forefront of Biosimilars in the regulated markets. It was early into identifying the opportunity way back in 2008 and invested in the same by divesting its legacy Enzymes business. It was also early into partnering with Mylan in 2009 & 2013 and then with Sandoz in 2018 to develop & commercialize the same. It was also among the very first company globally to launch products in US and has launches planned for atleast one product every year till FY25, post which Phase-II products from Sandoz partnership would start coming out.

Each biosimilar product is atleast $1 billion and more in market size with only 3-4 players competing max. This provides for a very rewarding proposition.

Biocon has scaled its biosimilars business from ~280 crores in FY15 to nearly ~2800 cores in FY21. So, everything looked promising. However, over last many quarters the company has done poor on execution front for varied reasons and there has been some major events like removal of biosimilars business CEO, product approval delays and quashing of ambitious $1 Billion target for FY22.

Because of repeated poor performance, I decided to exit the same. In the hindsight, I should have exited much earlier at the very beginning of 2021 when the CEO removal happened and Guidance was revoked. But I got biased by the business potential and failed to follow my framework of trend following which indicated an exit Jan’21 itself. I kind of went into value investing framework here as Biocon continued to become more valuable. At ~40,000 crore market cap, Biocon is very tempting as Biocon Biologics (75% stake) itself was recently valued at ~38000 crores in Serum Deal, Syngene (70% stake) is valued at ~22000 crores and then you have other tangible business of small molecules and various other intangibles of novel drugs.

But value investing is not my framework and it has never worked for me.

Syngene-

Thesis on Syngene was that you have a large discovery & development business which was now being complemented with a manufacturing piece. And manufacturing is the most rewarding part of a CRAMS business given that the uncertainty is lowest as the drug has been approved. I believed that Syngene was very well placed as having a large discovery & development business would act as a natural funnel for its manufacturing business and thus manufacturing scaleup would happen fast and that Syngene’s moat would strengthen by having a capability to cover entire spectrum of a drug’s journey over its patent life.

However, here again the execution has been very slow. Not only has manufacturing piece taken very long to setup, but the commentary also is not very encouraging on Syngene’s ability to secure projects for the manufacturing asset from its existing research business.

But that itself was not an exit decision for me, because even in base case Syngene can grow at low double digits on the back of research business itself. And upside potential is always embedded in a CRAMS business which one can never anticipate and could come out of nowhere.

But relatively I felt there were better opportunities available and thus I decided to replace the same.

Canfin Homes-

In lending, after Gold Finance, Housing finance is something that I like the most. It is secured and has the lowest default levels given the whole sentimental attachment to houses in India. Plus, the growth is relatively easier to get as the market size is huge and given that these loans are very long term in nature like atleast 5-7 years, the incremental disbursements continue to add up.

Canfin is one of the best franchises here with great track record of good asset quality & lending. Over last several years, growth was something that was lacking here and now the management is talking and pushing for growth even if that comes at slight moderation for profitability. And with real estate heating up, opportunity looks ripe.

I even get a sense that this whole push towards growth is because Canara Bank wants to exit this and they won’t sell it cheap.

Even though the market is becoming very competitive with very low rates offered by Banks, Canfin has the ability to compete with them as far as cost of funds is concerned and even at current profitability it can generate a good ROE of 15%+.

RACL Geartech-

I had touched upon RACL Geartech in my earlier post- Investing Dilemma.

It is a small company with ~200 crores revenues and has done ~100 crore capex in last 3 years with another ~50 crores in FY22, which is very aggressive for a company of its size. The company caters to premium auto products in exports market and does not do mass market products.

The only reason why I avoided this earlier was that I could not make sense of its accounting around cashflow statement (which I cannot even now) and did not want to get in a situation wherein promoter might be doing some financial engineering.

However, sometime back the promoters had an analyst meet with a fund and the way they conducted that meet showed sheer commitment of transparency & fairness towards minority shareholders, which is something I had never seen in case of any other company. This negated my reservations around earlier issue and thus I invested in the same.

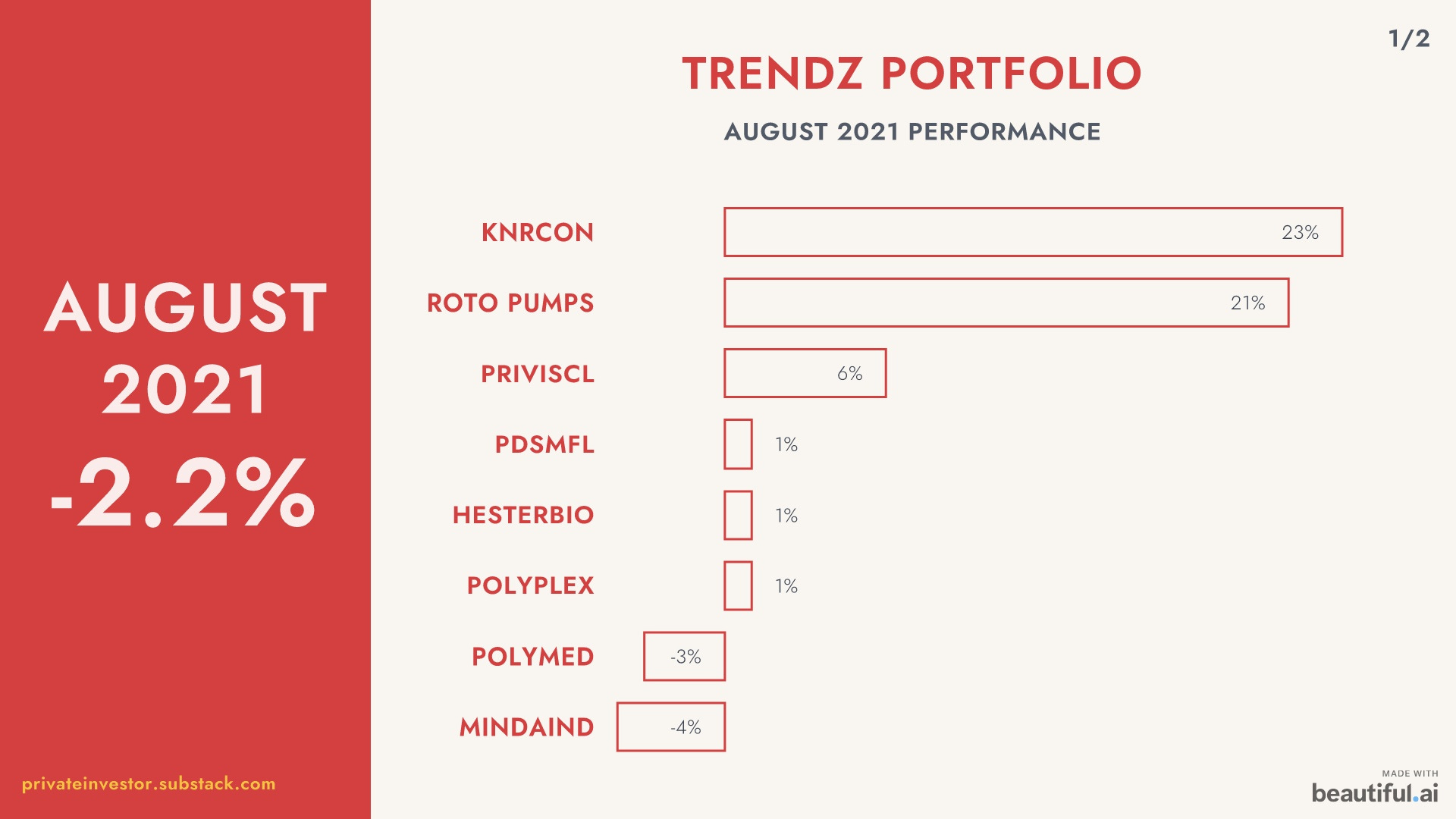

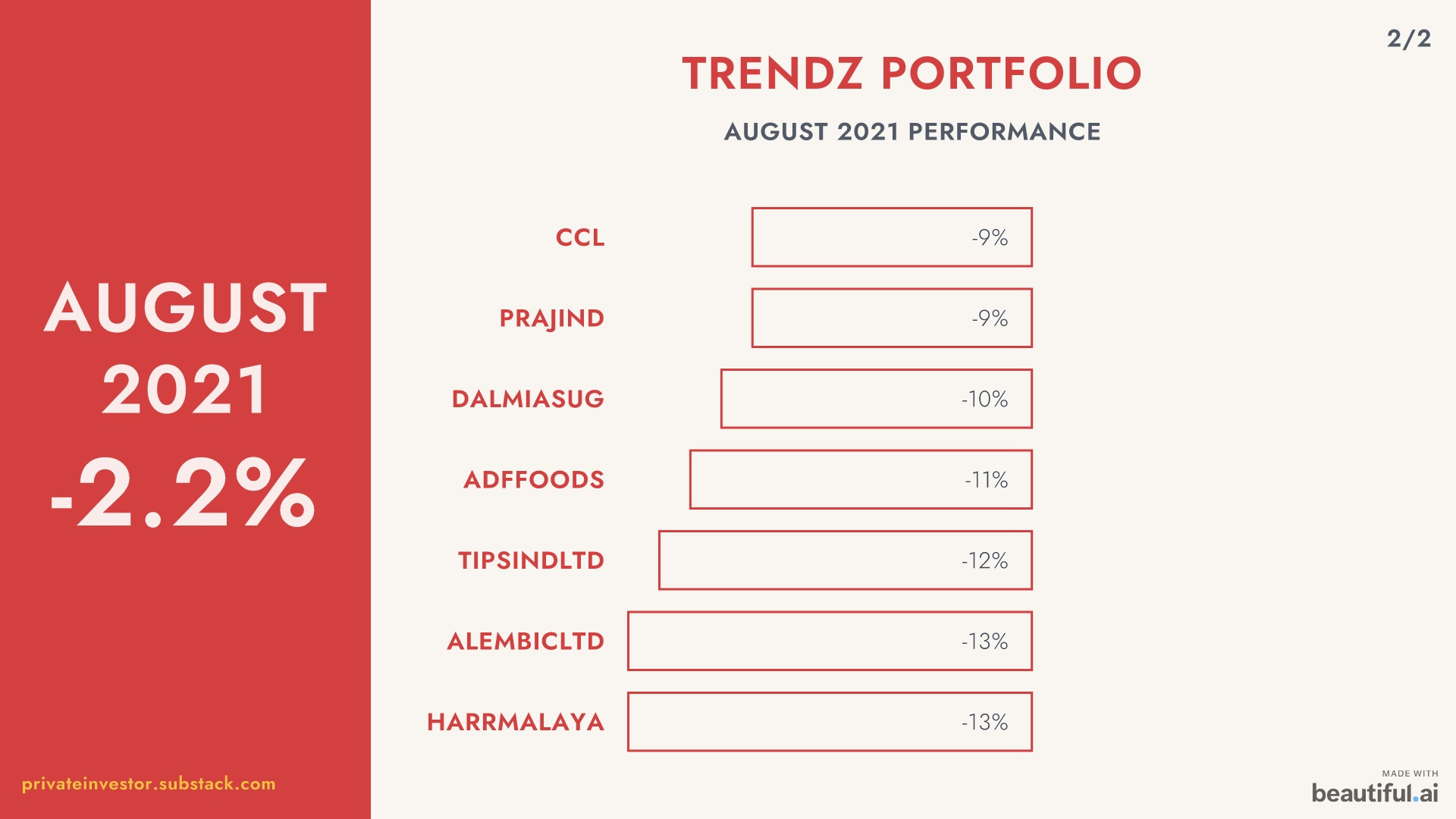

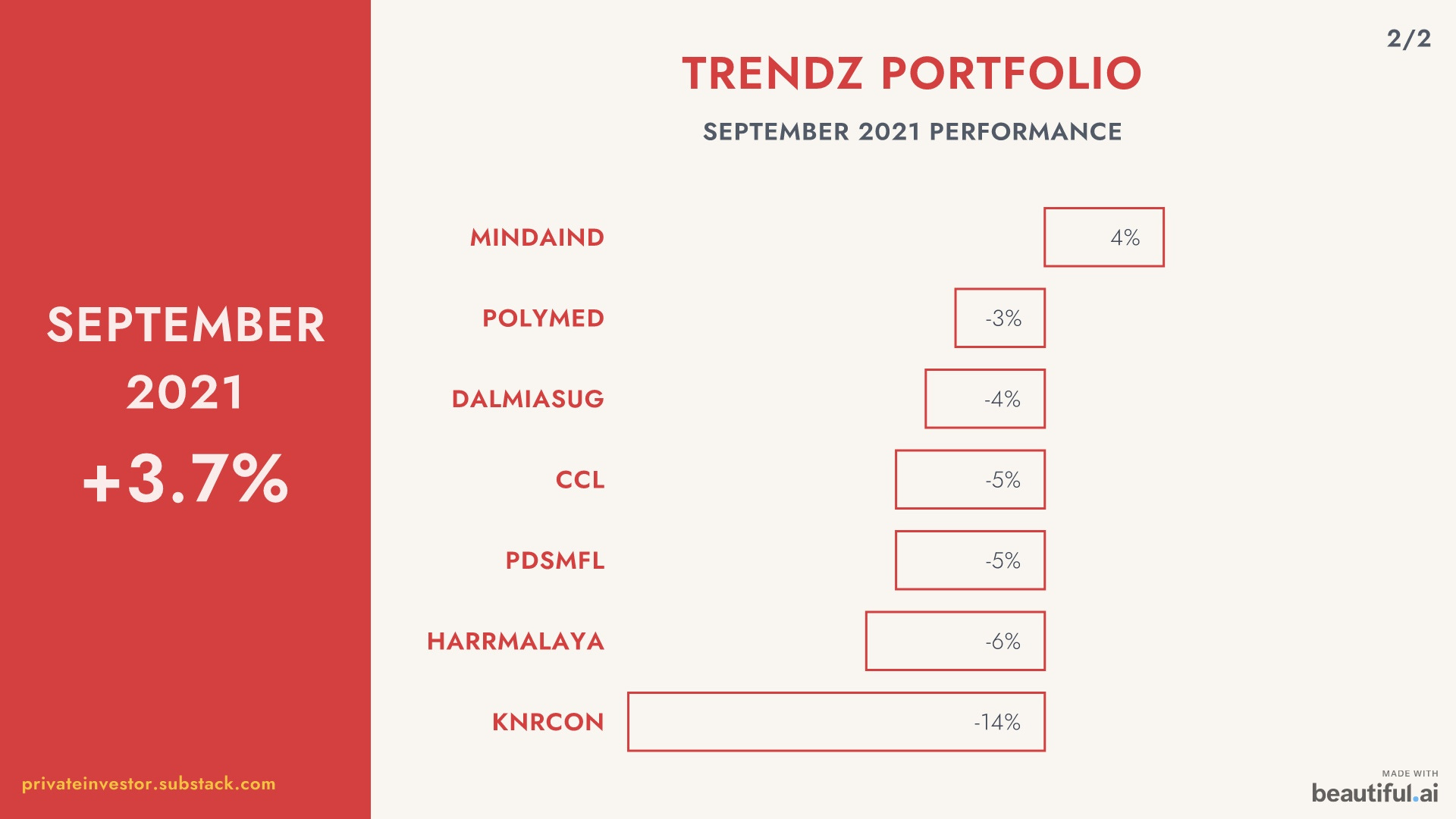

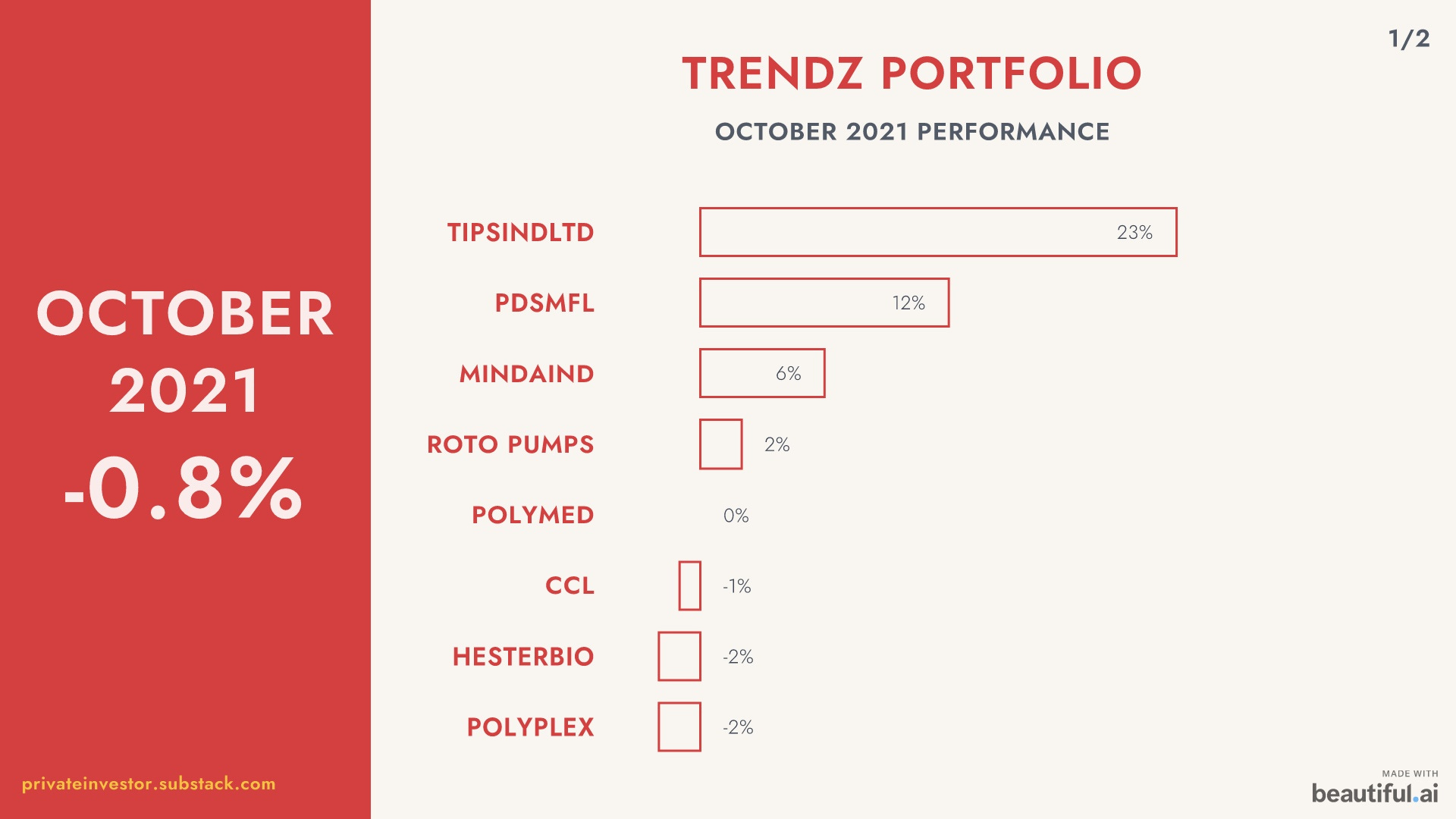

TRENDZ PORTFOLIO

August’21- Exited ALEMBICLTD. Added HCLTECHSeptember’21- No ChangeOctober’21- Exited ADFFOODS & HARRMALAY. Added BHARTIARTL & OBEROIRLTY

That’s All For This One

02/11/2021

Great insights Ankush, just a question on Syngene exit, so what is the specific reason you found out where we can see the company is not getting deals for the manufacturing facility, one question is what is the revenue Potential post the CAPEX completion by the company any insights on the same.

As always good write up and portfolio update.....While the exit from Biocon is convincing as despite best efforts , biosimilars are unable to make much headway and market shares continues to be single digit... exit from syngene is a bit surprising as company may still deliver a decent growth with manufacturing may come as an added optionality....