Optionality Of Cash

How Cash In some situations can create multiple times its current value in Market Cap

Hey! There are multiple patterns that can play out in stocks. These patterns overtime have become a playbook of sort for investors to form their core thesis for a particular stock.

Branding Plays- Identify stocks that are dealing largely in commodity type space but are investing heavily into branding which overtime will allow the company to garner more market share and also charge a premium. Overtime this allows for improving efficiencies with a dominant market positioning which also provides for valuation re-rating and thus makes for a great pattern to watch out for in stocks. Historical examples of this playbook have been Relaxo and Astral Pipes. A recent example of the same has been APL Apollo Tubes.

Big getting Bigger- This playbook centers around the idea that companies that have dominant positioning in a market will continue to be at an advantageous position due to their dominant positioning and will incrementally get bigger and bigger. This idea I believe is at the center of Consistent Compounders strategy.

Execution Plays- Here the bet is on the management who have displayed strong execution capabilities that has resulted in the company achieving a competitive positioning in a crowded space; and expecting that they will continue to do so in more and more areas. Deepak Nitrite and Laurus Labs are two of the finest examples of such plays.

Optionality Plays- This is something I have talked about in detail in my previous blogs- Investing In Complexities, Non-Linearity and Optionality and How To Find & Evaluate Complex, Non-Linear and Optionality Opportunities. And this is the playbook I am most interested in.

In this post, I am going to talk about an additional source of Optionality- CASH

The way market values stocks (which is primarily based on earnings power), cash is hardly given any value from the market capitalization’s perspective. If a company has say Rs1000 crores cash on the balancesheet, that would never be valued at more than 1x, ie. Rs1000 crores in cash would mean max Rs1000 crores in market cap. In most cases, it is not even 1x, it would be way less than that.

The exception to such scenario is obviously distressed companies wherein there is hardly any earnings power and market’s primary focus is on survival and thus Cash is king in such situations and is valued heavily. So, if Voda-Idea suddenly has Rs10,000 crores cash, that would easily add Rs10,000 crores in market cap if not more.

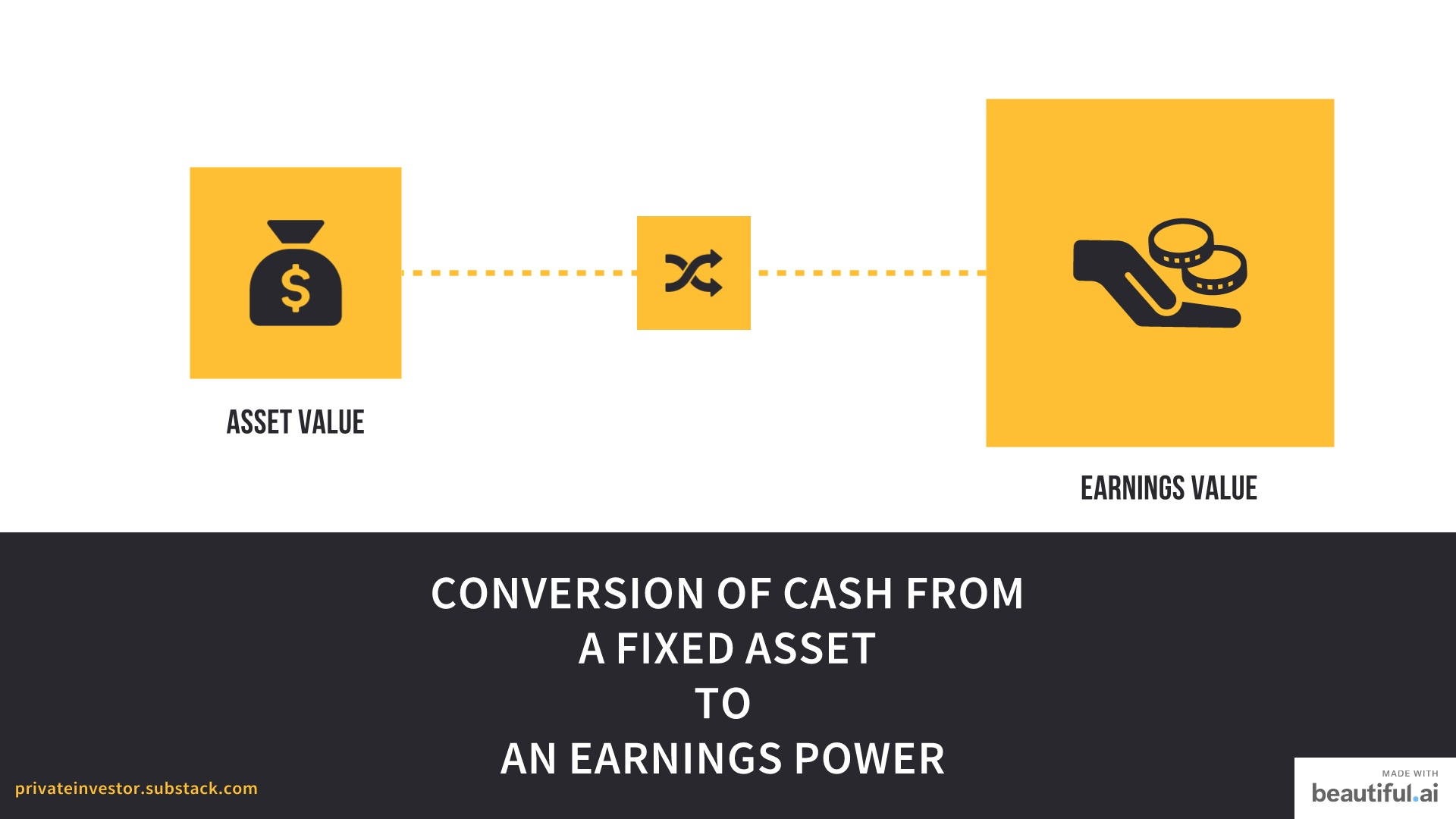

But Cash in certain conducive conditions can be a big optionality that can create market capitalization in multiples of its value ie. Rs1000 crores Cash can create even 5000-10,000 crores in additional market cap.

Let me explain the same with an example and then talk about the specific conditions that are needed for such optionality to play out.

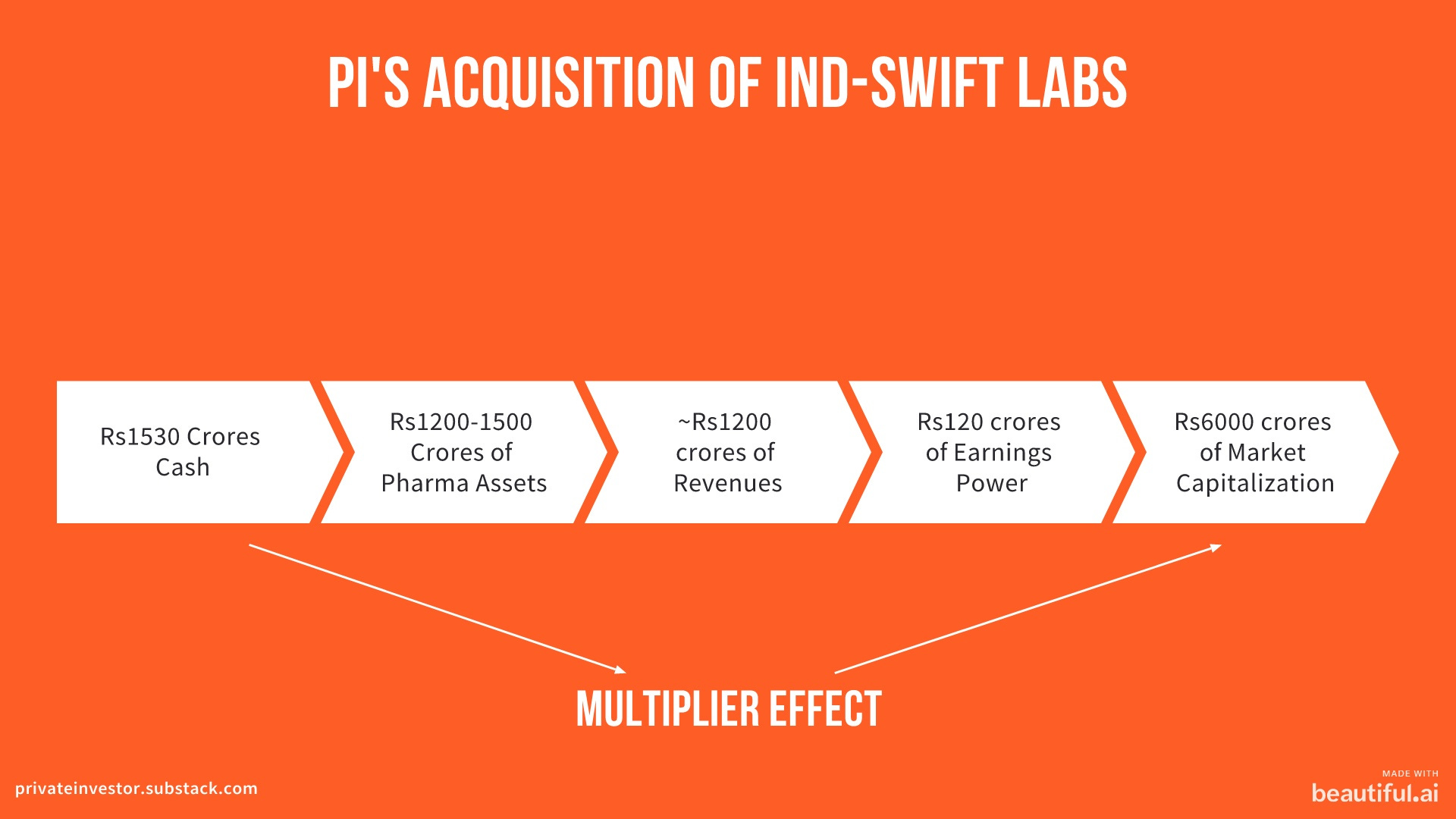

PI Industries recently announced acquisition of Pharma API & Intermediates business of Ind-Swift by using Rs1530 crores of cash sitting on PI’s balancesheet. The acquisition will provide PI with ~1200-1500 crores of Pharma manufacturing asset base.

These assets have potential to generate atleast 1x asset turn ie. Rs1200 crores in revenues (Pharma assets can generate anywhere from 1.5-2x Asset Turn on Gross basis). The margin profile of Ind-Swift Labs as it sits now is ~10% after adjusting for the huge interest cost that would not be there for PI given that they are acquiring the business on debt free basis.

So, PI can generate ~120 crores (1200 crores X 10% Margin) in post-tax profits from these acquired assets. Now this is where the optionality kicks in, PI which is currently valued on its earnings power is trading at >50 times its post-tax earnings. At this valuation, the additional Rs120 crores of profits can add ~6000 crores (120*50) in market cap for PI. So essentially the cash that was being valued at 1x or less its value of Rs1500 crores can now add a value of ~6000 crores, ie. 4x multiplier.

And this is a very base case without considering any improvements in efficiencies that would be brought by PI.

Based on my understanding of PI’s capabilities and some thoughts provided by the management in the recent concall, the margins for the acquired Ind-Swift business should grow to mid-teens and the value addition by this Rs1500 cash could in multiple of 7-8x for PI.

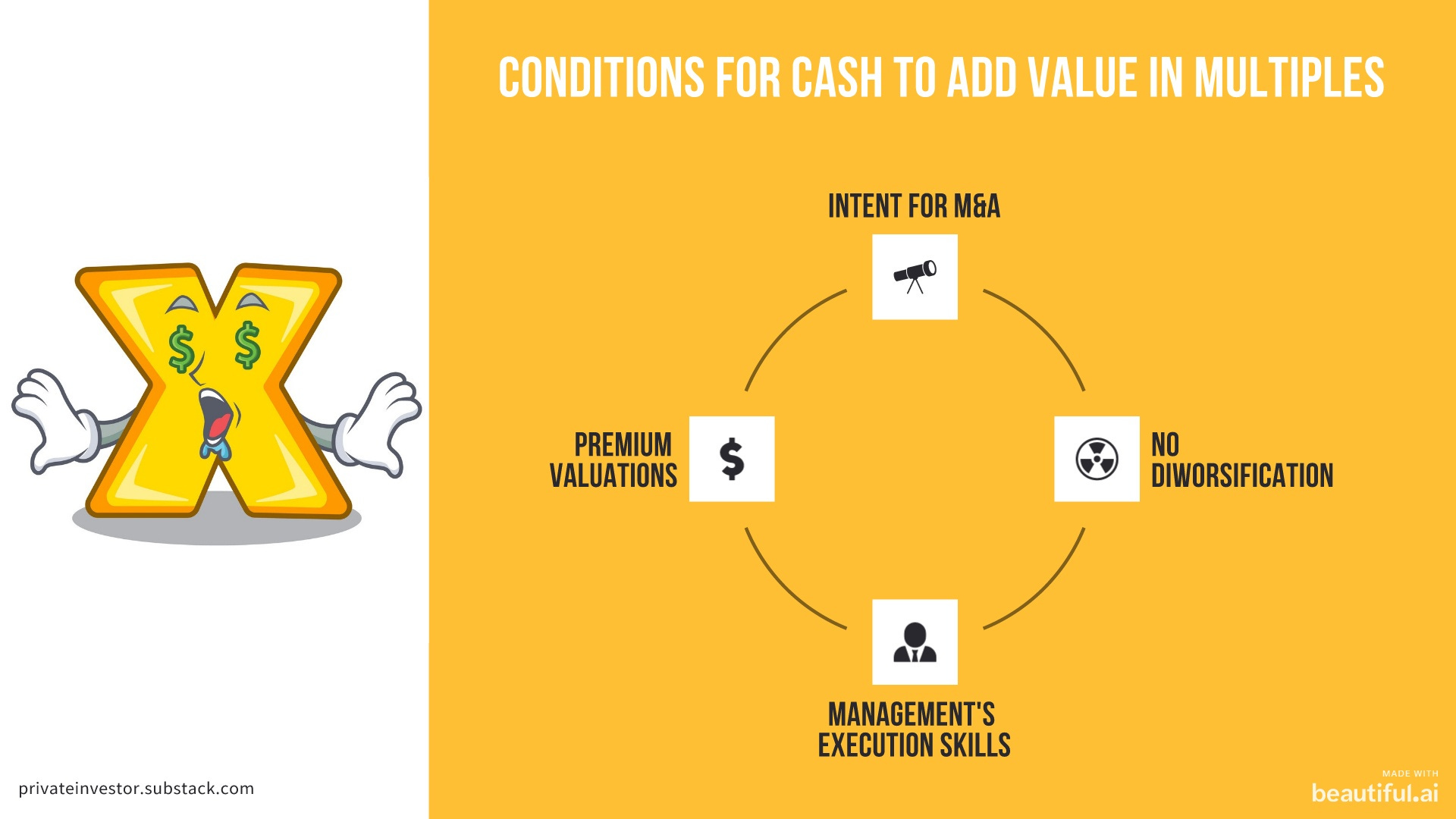

Now having understood how Cash can provide some optionality by creating market cap in multiples of its current value, one also needs to understand that this will not work in every situation. You cannot expect that every company that is having cash on its balancesheet will realize such Optionality of Cash.

1. Intent for M&A (Mergers & Acquisition)

The primary condition for Cash to create Optionality is a clear intent by the company of a possible M&A. In my How To Find & Evaluate Complex, Non-Linear and Optionality Opportunities post, I had highlighted that timing is key for any kind of optionality play. There are many companies that have decent amounts of Cash on their balancesheet, but that itself does not mean that they will end up using that cash for some acquisition.

PI Industries last year raised Rs2000 crores with the sole purpose of acquiring some new manufacturing assets (primarily on the pharma side) and also had a clear timeline to complete such M&A within 18-months by Dec’2021, so monetization of PI’s cash was imminent.

2. No Diworsification

Diworsification is the bad brother of Diversification. Diworsification leads to a situation wherein instead of adding value, the acquisition destroys value. So, buying Hotels would not create the multiplier effect of cash (ITC Meme! 😁).

What you should basically look for is an acquisition that is in a similar line of business or something that builds up on the existing capabilities of the company while keeping the profitability & capital efficiencies (ROCE) of existing business intact; if not improve.

And the reason why this is important is that a M&A into another business would pose challenges in terms of integration & execution and might not be able to provide the same level of profitability & capital efficiency. Further, a diversification into a different business also possesses some challenges in terms of valuations; markets typically value a company with varied lines of business lower than what it would value those same businesses if they would have been listed separately.

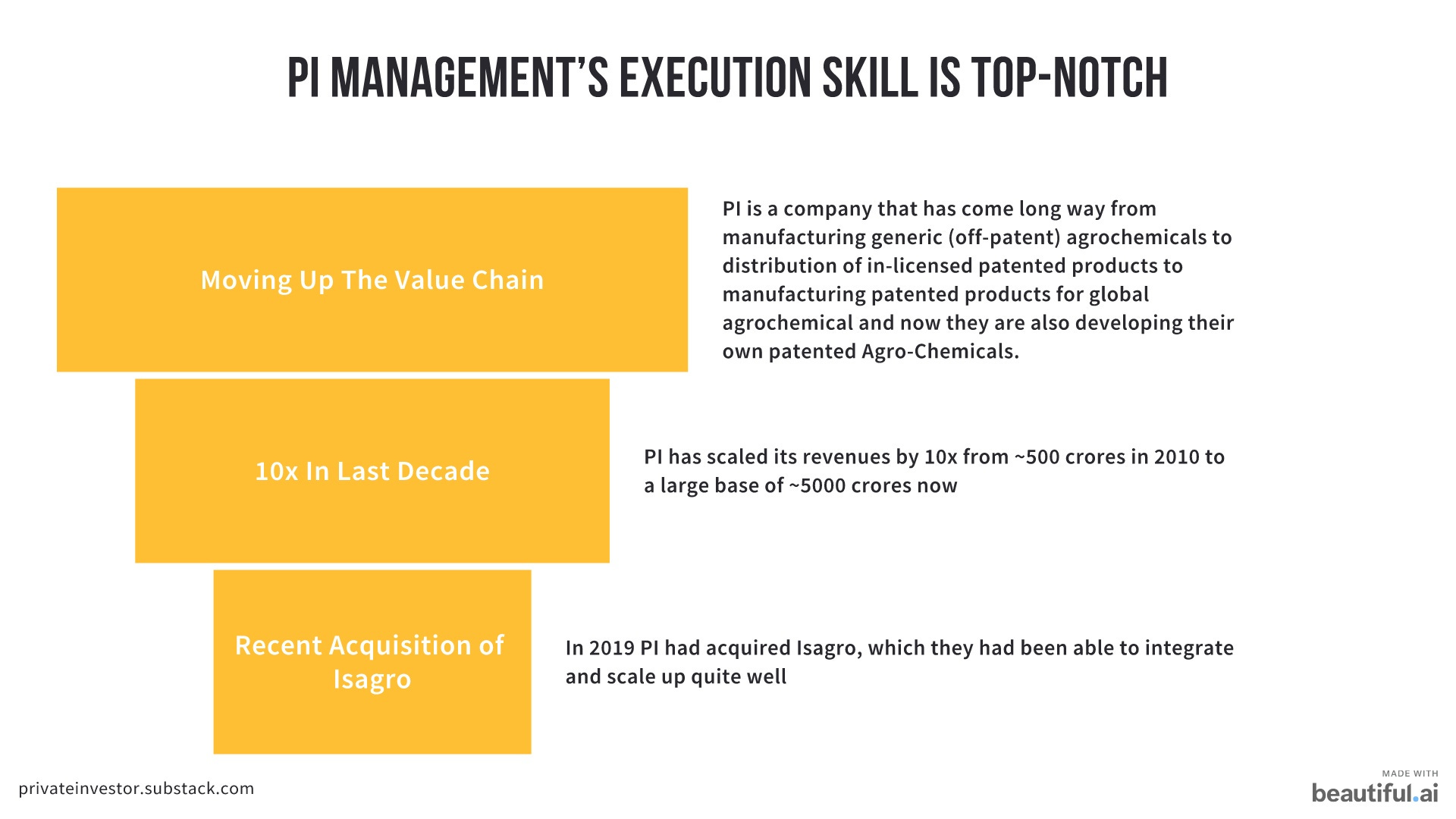

In case of PI this acquisition is an extension of company’s business into a larger market. PI has an extensive experience is manufacturing of agrochemicals on a large scale for global markets and has rich experience in working with innovator companies to provide large scale manufacturing services. Pharma API & Intermediates itself is a chemistry led manufacturing business that involves doing large scale manufacturing for global markets but with more regulatory oversight and R&D skills.

PI itself has been working on its own R&D to develop products for the Pharma space by leveraging its chemistry know-how that it has gained over the years doing manufacturing work for the Agrochem innovators. In fact, last year PI has already started supplying intermediates for one of the Covid related drug.

So, this acquisition is a fast-tracked entry into the pharma space which PI has already been working on.

3. Management’s Execution Skills

This point is an extension of above point. Even if there is no diworsification, integration of a similar business itself is a challenge that requires great execution skills. Plus, in order to generate value out of an acquisition one also has to improve the state of the acquired asset. Buying something worth Rs100 for Rs100 or even less does not add much value, real value addition happens when one is able to increase the value of the acquired asset to more than what you paid for it. And this all depends on management’s execution prowess.

4. Premium Valuations

This is one of the key aspects of this entire Cash Optionality. So, cash is valued as an asset at its face value or even less by the market, but when this cash is used to acquire something, you are essentially converting the cash from an asset to an earnings power. And the value of this earnings power is directly dependent on the valuation that a company trades at. So, a P/E (price-to-earnings ratio) of 10x means that the market is giving a value of 10 times the earnings power and thus higher the valuation, higher would be the multiplier effect of Cash’s conversion from an asset to an earnings power.

PI along with companies with similar quality & scale like Syngene, Divis Labs and Gland Pharma, all trade at 50-60x their current earnings. So, the increase in earnings power that this acquisition will add to PI, will create value which is 50-60x times such earnings power.

This obviously will work under the assumption that the valuations do not de-rate due to the acquisition. But if the above two points of No Diworsification and Management’s Execution Skills checks out, then there is a good probability that valuations will not suffer due to an acquisition.

So, this is how Cash in some conducive situations can act as an Optionality and add some good value to a company’s market capitalization. In case of PI, the Ind-Swift acquisition as it sits today without any value addition by PI will add ~90 crores in earnings power and thus ~4500 crores in value (90 crore PAT * 50x PE Multiple), which is ~10% of PI’s current market cap.

Based on PI’s management commentary in the recent concall, I believe that PI will quickly scale this business to mid-teens kind of margins with increased topline and the value addition would be much higher. Some of the plans put forth by PI-

1. There are a lot of untapped opportunities in Ind-Swift’s existing product portfolio which PI will look to cater with better commercial excellence. (Revenue Improvement)

2. Within 18 months, the goal is to bring Ind-Swfit’s operations in a steady state with optimum working capital requirements and incorporate PI’s execution excellence. (Improved Capital Efficiencies)

3. Induct products from PI’s own Pharma R&D pipeline into Ind-Swift and also increase the share of Ind-Swift’s CRAMS business (currently small part of Ind-Swift’s business), which is a high margin business. (Margin & Revenue Improvement)

GLAND PHARMA is another company that has large amounts of Cash on its balancesheet and is also actively looking for M&A opportunities and also checks all the four points we discussed above. Gland currently has ~3000 crores of cash which it is looking to use to acquire assets to enter into more complex products within its current business of Pharma Injectables. Any M&A here would have extremely high multiplier effect on Cash given that Gland has high net margins of ~30%. So, earnings power that would be generated from monetization of cash would be very high which when combined with rich valuations of 50-60x could add substantial value to Gland’s market cap. I had earlier shared my thoughts on Gland Pharma in my last Journal.

Another company that can witness Optionality from cash in some future would be Natco Pharma. As highlighted in my Natco Blog that Revlimid opportunity would generate substantial cashflows for Natco and given the management pedigree at Natco, I am quite sure that they would use the cash for create some large optionalities.

Finally, this framework is something that can be an add-on to your primary thesis on a particular stock and not something that itself can become the primary thesis. This is because the optionality here would not be something very big in relation to company’s existing market cap (maybe 10-30% kind of value addition). But it is something that would act as an upside point in your overall thesis.

Excellent concept clarity on the subject...

Love your thesis. I think how the optionality plays out is mostly dependent on the execution power of the management. So far, PI Industries management had shown great resilient power and hope they will deliver again with this acquisition. Great analysis Ankush. Thank you for sharing.